Best Savings Accounts That Give You Bonus Interest For Having A Mortgage

A big part of our financial planning, perhaps even the foundation of it, comes from our savings. They provide the reserves for our cash flow, and they also ensure we have something stored up to use for higher aspirations or a rainy day.

At the same time, savings represent the most basic form of wealth growth you can have, as long as you haven't kept your money in biscuit tins under your bed.

How Savings Accounts Work

Savings are stored with banks in savings accounts, which pay a certain amount of interest every year, helping your savings to grow.

There are many kinds of savings accounts in the market today, from basic savings accounts, to fixed deposit accounts which offer a higher interest rate if you do not touch the savings for a period of years, to "multiplier" type accounts which offer progressively higher tiers of interest, or cashback rebates, that you can "unlock" by carrying out certain kinds of payments and transactions to and from that account.

Popular High-Interest Savings Accounts in Singapore

Of the above, the "multiplier" type savings accounts are the most popular as they offer high bonus interest rates. Some of the most popular ones currently are:

DBS Multiplier account

Maybank Save Up Programme

OCBC 360 account

UOB One account

Standard Chartered Bonus$aver account

How Mortgages Can Help Your Savings Rate

One of the main ways you can "unlock" higher savings rates if you use a "multiplier" type account, is through regular transactions, such as crediting your income into it, or paying your monthly bills from it, or simply shopping online with it.

Another way to get a higher interest rate that might be more of interest to you, is simply by having a savings account with a bank that rewards you with bonus interest if you also have a mortgage with them! The banks that provide this transaction option are DBS and Maybank, and we'll take a look at their savings accounts and what they could do for you.

Disclaimer: As we emphasize again at the end of this article, do not choose your mortgage based solely based on savings accounts! In contrast with a six-figure home loan, the few hundreds in bonus interest is trivial. Treat this more as icing on the cake.

1. DBS Multiplier Savings Account

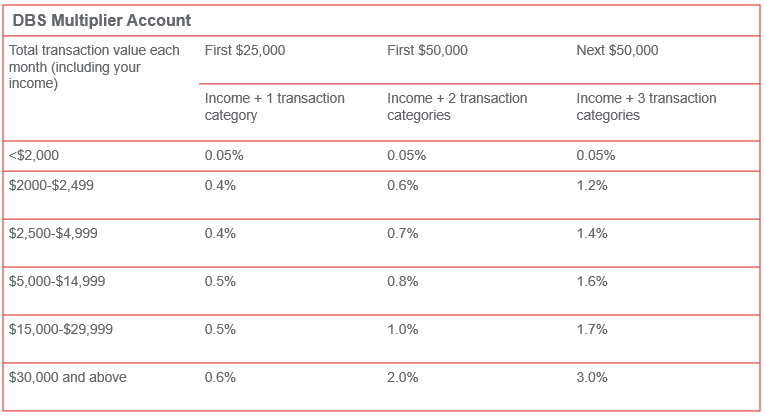

The DBS Multiplier is a savings account that qualifies you for a higher savings rate if you credit your income of at least $2,000 a month into the account, and carry out at least one of the following activities:

Transact with DBS in at least one of the following categories: credit card, home loan, insurance, and/or investment

Carry out transactions with Paylah, for those without any of the above

The DBS Multiplier Account interest rate scales depending on how many categories you transact in, how much your transactions are (including income), and how much you have in your account, up to a maximum of $100,000. The more you transact with DBS, the more interest you stand to earn compared to a standard interest rate of 0.05% if you stored your money in an ordinary savings account.

Note: The above is accurate at the time of writing. For the most updated information, check DBS's website.

Find it hard to understand? Here are some examples to better illustrate how the interest is earned.

Scenario 1: Fulfilling both requirements

So for instance, if you:

have $32,000 in your account and credit your $2,000 salary each month

also pay for a DBS credit card from this account

carry out about $4,000 worth of transactions (including salary credit) a month,

you have unlocked the first tier and an interest rate of 0.4%.

However, this 0.4% will only be given to $25,000 of the $32,000 in your account, as the tier only covers the first $25,000 in your account. The remaining $7,000 will only earn the basic 0.05% interest rate.

Scenario 2: Fulfilling only one requirement

Let's say now that you:

have $50,000 in your account and credit $2,000 of your salary each month

still only transact in one category (your credit card) as well as your income

still carry out about $4,000 worth of transactions a month.

In that case, you have not fulfilled the requirements for the second tier, and are only eligible for the benefits of the first tier.

You would earn 0.4% on the first $25,000, and a basic interest rate of 0.05% on the remaining $25,000.

Scenario 3: Unlocking the next tier

Let's say now that you:

have $50,000 in your account and credit $3,000 of your salary each month

you transact in two categories: your credit card and home loan

you carry out about $6,000 worth of transactions a month.

In that case, because you have transacted about $6,000 and in two additional categories, you earn 0.8% interest. Since you only have $50,000 in the account, you earn this bonus rate for all your savings.

In the case that everything stays the same but you have say, $75,000 of savings, then the balance of $25,000 will earn the base rate.

2. Maybank Save Up Programme

Like the DBS Multiplier account, the Maybank Save Up Programme rewards you for being a Maybank customer, by offering you bonus interest rates per month on top of the basic interest rate of up to 0.3125% per annum, depending on many Maybank transactions or products you have active that month. If you have a home loan with Maybank, this would count as one transaction.

Number of Maybank transactions | Bonus interest added to basic rate (calculated monthly) |

1 | 0.3% |

2 | 0.8% |

3 | 2.75% |

There are nine categories of transactions that are counted as bonus interest. Different transactions and products are counted for different lengths of time. For example, a transaction that has a bonus interest period of three months will give you bonus interest for three months before the bank checks again - and if it's still active at the end of that period, your bonus interest from that transaction is extended for another three months.

A Maybank home loan would guarantee you 12 months of bonus interest - in other words, it means permanent bonus interest for your savings as long as you stay with Maybank.

Minimum amount | Bonus interest period | |

Salary Crediting | $2,000 credited monthly | 1 month |

GIRO Bill Payments | $300 paid monthly | 1 month |

Maybank Credit Card | $500 spent monthly | 3 months |

Structured Deposits | $30,000 deposited | 12 months |

Unit Trusts | $25,000 cash investments | 12 months |

Premium Insurance | $5,000 in annual premiums | 12 months |

Home Loan (excluding equity/cash-out loans) | $200,000 total | 12 months |

Car Loan | $35,000 | 12 months |

Renovation Loan | $10,000 | 12 months |

Education Loan | $10,000 | 12 months |

Again, let's use some examples to make sense of all the above information.

Take for example that...

You have $26,000 in your Save Up account,

are crediting your salary of $2,000 a month to the account,

and that you are the primary holder of your house's $300,000 Maybank home loan.

Based on this, you are eligible for a bonus interest rate of 0.8% as you have 2 products or services with Maybank. This gives you an interest rate of 0.3125% + 0.8% = 1.1125%.

Over one year, your $26,000 would earn $289.25 in interest. By way of contrast, a regular Maybank savings account would give you a rate of 0.1875%, meaning you would have only earned $48.75 in the same period of time if you had saved your $26,000 in an ordinary Maybank savings account.

Maximising Your Savings Returns from Your Mortgage

The right savings account can help you to get more from your mortgage, but as you can see from the case studies above, the earnings in interest are not huge, unless you have enough savings to unlock the highest tiers, and even then, the earnings only apply to the amounts covered by the tier.

This means if you're in the process of shopping for a mortgage, you shouldn't be choosing your home loan based on what affiliated savings accounts are available, except in very specific cases where two potential choices are evenly matched and this small factor tips the balance.

However, if you do already have a "multiplier" savings account with a bank that gives bonus interest to borrowers, then it may be worth considering taking up a home loan with the same bank in order to unlock even more tiers of interest.

Either way, when you're comparing mortgages for your next property or refinancing, you need to do a careful calculation for the costs and benefits for the mortgage, and then for different combinations of savings accounts, if you wish to factor that into your decision making. You'll also need to weigh your own priorities and ensure that the combination you choose will suit your needs and lifestyle.

If you need help and advice on deciding on your mortgage, or if you're considering refinancing, come speak to our Home Finance Advisors at PropertyGuru Finance, and we'll help you find the best way forward!

Disclaimer: Information provided on this website is general in nature and does not constitute financial advice.

PropertyGuru will endeavour to update the website as needed. However, information can change without notice and we do not guarantee the accuracy of information on the website, including information provided by third parties, at any particular time.Whilst every effort has been made to ensure that the information provided is accurate, individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial planner or your bank to take into account your particular financial situation and individual needs.PropertyGuru does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this website. Except insofar as any liability under statute cannot be excluded, PropertyGuru, its employees do not accept any liability for any error or omission on this web site or for any resulting loss or damage suffered by the recipient or any other person.