Time to wrap up. The FTSE appears to have closed basically flat, marking its worst month since March (and worst week since June). These were some of the day’s top stories.

Jack Ma’s Ant Group float attracts bids worth $3 trillion: Jack Ma’s Ant Group has attracted at least $3 trillion of orders from individual investors for its dual listing in Hong Kong and Shanghai – enough to buy JPMorgan 10 times over.

Thanks for following along today. We’ll be back on Monday – have a great weekend!

04:05 PM

Marriott hack fine cut to £18m

The Marriott hotel group has been fined £18.4m by the Information Commissioner’s Office (ICO) over a 2014 hack which saw records of 339 million guests stolen by hackers.

My colleague James Cook reports:

The fine is a significant reduction from the initial £99.2m fine that the ICO announced last year.

Hackers broke into the database of Starwood Hotels in 2014 and stole information including email addresses, phone numbers, passport information and loyalty programme numbers of guests. Seven million records in the breach related to people from the UK, the ICO has said.

Marriott bought the Starwood group in 2016 and the breach was only discovered in 2018, four years after the hackers had accessed the systems.

The fine only covers the period from 25 March 2018 when new GDPR rules came into effect. The ICO reduced the final fine because of the steps the company took to deal with the incident as well as the impact of the coronavirus pandemic on the business.

After a sharp drop yesterday that took its price beneath $37 per barrel for the first time since May, Brent crude has narrowly extended its losses today amid rocky trading:

03:06 PM

Market moves

With just over an hour of trading left, European equities remain moderately in the red. Wall Street is having a worse time as tech stocks drag.

02:25 PM

Walmart pulls guns from shelves ahead of US election

Walmart

Walmart has removed guns and ammunition from its shelves as it prepares for the possibility of civil unrest or looting following Tuesday’s US presidential election.

My colleague Joe Curtis reports:

The move is designed to protect customers and employees amid rising tensions as voters choose between Donald Trump and Democrat challenger Joe Biden to be their next president.

“We have seen some isolated civil unrest and as we have done on several occasions over the last few years, we have moved our firearms and ammunition off the sales floor as a precaution for the safety of our associates and customers,” a Walmart spokesman said.

Walmart sells guns and ammunition in around half its 5,000 stores around the US and will continue to do so upon request, it added.

The retailer made a similar move in June at the height of widespread protests over the death in custody of unarmed black man George Floyd.

US stocks have dipped at the open, with the Nasdaq taking the hardest hit and heading for its own worst week since March.

Bloomberg TV - Bloomberg TV

01:10 PM

PwC commits to keeping offices

PwC - Jack Taylor/Getty Images

PwC has committed to retaining all its office space despite the rise of home working during the pandemic.

My colleague Ben Gartside reports:

The big four accountant’s UK chairman, Kevin Ellis, said that while hybrid working was here to stay, he believed the office would remain a key part of working life.

"The pandemic has accelerated changes to working patterns, bringing things forward by three or four years. Hybrid working is here to stay, and therefore the office will remain a key part of working life.”

European markets are currently moderately in the red, with that worst week since March title looking locked in currently.

There’s just over half an hour until the US open – currently, futures trading is posting toward a sharp drop on Wall Street in the wake of last night’s mixed tech results. The S&P 500 is currently set for a 0.7pc drop, while futures on the tech-heavy Nasdaq are down 0.9pc.

12:39 PM

Exxon sinks to $680m loss

ExxonMobill - AP Photo/Richard Drew, File

Oil giant ExxonMobil has warned it could take up to $30bn in writedowns on its natural gas assets after posting a historic loss.

Exxon is confronting one of its biggest crises since Saudi Arabia began nationalizing its oilfields in the 1970s. The company lost $680 million, or 15 cents a share, during the third quarter, compared with the 25-cent per-share loss forecast in a Bloomberg survey of analysts. The shares fell 1.2pc in pre-market trading.

That was in stark contrast to Chevron Corp., which disclosed a surprise profit despite a gloomy outlook and the lowest crude and gas output in more than two years. European supermajors Total SE, Royal Dutch Shell and BP also turned in better-than-expected third-quarter performances.

Blindsided by the economic fallout from the Covid-19 pandemic, Exxon Chief Executive Officer Darren Woods abruptly ditched an ambitious rebuilding effort and imposed widespread job cuts that are unprecedented in Exxon’s modern history.

If Exxon goes ahead with the write-down in Q4, the up to $30 bn impairment would be one of the largest ever in the oil industry, perhaps second to Conoco's $34bn writedown in 2009 (under CEO Jim Mulva) that included ~$25 bn from the Burlington Resources deal in 2005 | #OOTT

Mexico’s GDP rose by 12pc in the third quarter, adding to the growing list of strong summer rebounds.

Agriculture-linked industries drove much of the growth, with industrial and services sectors remaining weaker year-on-year.

The country recently conceded its death toll is higher than previously admitted. President Andrés Manuel López Obrador has been criticised for shunning face masks and encouraging Mexicans to break social distancing guidelines.

11:49 AM

Jack Ma’s Ant Group draws $3 trillion in bids for float

Jack Ma’s Ant Group has attracted at least $3 trillion of orders from individual investors for its dual listing in Hong Kong and Shanghai – enough to buy JPMorgan 10 times over.

My colleagues report:

Bidding was so intense in Hong Kong that one brokerage’s platform briefly shut down after becoming overwhelmed by orders. Demand for the retail portion in Shanghai exceeded initial supply by more than 870 times.

The stampede is fueling predictions of a first-day pop when Ant is due to start trading on Thursday, even as skeptics warn of risks including the US election, tightening regulations in China and rising Covid-19 infections worldwide.

The Chinese fintech behemoth’s $35bn (£26bn) float represents a major vote of confidence in a company that could end up shaping the future of global finance. It also underscores the ability of Chinese firms to attract huge amounts of capital without tapping American markets, a win for Beijing as it tries to reduce its vulnerability to the threat of US financial sanctions.

Read more: Jack Ma’s Ant Group float attracts bids worth $3 trillion

11:13 AM

Eurozone GDP reaction: ‘Bittersweet’

Responding to this morning’s eurozone GDP reading, Bert Colijn from ING says it is a “bittersweet result”, adding:

The current level of economic output is far more interesting than the growth rate. At -4.3pc, below the peak in GDP of 4Q19, the rebound has still left a very significant gap to close. At levels of output, much below pre-Covid-19 levels and with new restrictive measures on the economy, concerns about second-round effects are growing.

This means that the focus will now turn to how adequate fiscal responses will be to counter the long-term effects of new partial lockdowns.

Daniel Bergvall from SEB said there are growing signs of weakness in the fourth quarter:

[These] numbers reflect the past as the present situation has clearly deteriorated going into Q4 as Covid-19 infections are gaining pace and countries are introducing new lockdown measures. Even if the current strategy is different from what we saw during the spring they will put a clear downward pressure on growth in the near term.

11:02 AM

Market moves

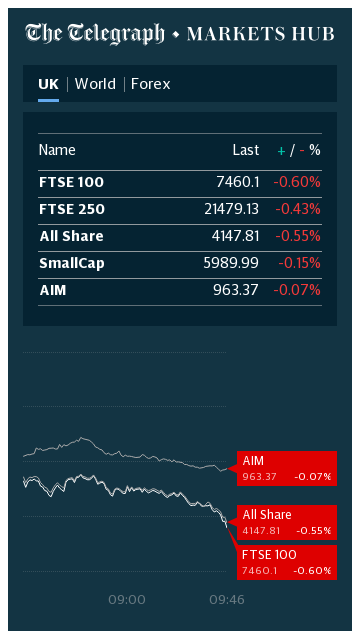

After choppy trading, European stock markets remain slightly in the red. The FTSE 100’s come under slightly more pressure as the pound pushes higher.

10:34 AM

Money round-up

Here are some of the day’s top stories from the Telegraph Money team:

The stamp duty holiday and pent-up demand after lockdown pushed 12-month house price growth to a five-year high of 5.8pc in October, new data shows.

My colleague Melissa Lawford reports:

The average British home cost £227,826 this month, a jump of 0.8pc from September, according to Nationwide building society’s house price index.

Homes now cost £12,458 more than they did a year ago. But experts have warned activity could stop “sharply” and pries could fall.

Robert Gardner, of Nationwide, said that the outlook for the market remained “highly uncertain” as unemployment rose and Britain’s economic recovery slowed.

The future of house prices would depend "heavily on how the pandemic and the measures to contain it evolve as well as the efficacy of policy measures implemented to limit the damage to the wider economy,” Mr Gardner said.

The eurozone economy solidly beat expectations for third-quarter growth, expanding a record-breaking 12.7pc in the third quarter.

The jump – which followed an 11.8pc decline in the previous three months – follows stronger-than-expected readings for all the bloc’s biggest economies as they bounced back from spring lockdowns.

European leaders won’t celebrate for long, however: the latest indicators for eurozone growth have turned negative, new lockdowns loom and European central Bank president Christine Lagarde has warned the outlook for November is especially grim.

It looks like things are going to be pretty touch-and-go with European markets today – the continent’s top indices are wobbling either side of flat, caught between poor sentiment and those expectation-beating GDP readings.

As things stand, the benchmark Stoxx 600 is set to drop 5.8pc this week, slightly worse than the 5.7pc fall seen in mid-June. Unless conditions improve, this is set to be the worst week since March.

09:20 AM

Italy smashes expectations with 16.1pc growth

Italy’s economy grew a mighty 16.1pc in the third quarter, beating expectations solidly.

After becoming the first European country to suffer a widespread outbreak of the virus, Italy’s economy shrank 13pc in the second quarter, a large measure of which has now been recovered.

But like so many other European countries, it is now gripped by a second wave which has cast a shadow over the prospects for a continued recovery:

09:10 AM

German growth beats expectations

Germany has joined the string of expectation-beating third-quarter GDP readings, with growth of 8.2pc during the third quarter.

Following beats for Spain and France (and Italy, which I’ll get onto shortly), it now looks certain that the eurozone will have beaten growth expectations in the third quarter. The real challenge now is the fourth, particularly the grim November that looms.

Germany, which contained its first virus wave effectively, was comparatively lightly hit in the second quarter. However, having imposed a ‘light’ lockdown for the coming month, it looks like Europe’s biggest economy could face a double-dip output fall.

08:54 AM

FTSE flattens out

The FTSE 100 has pulled back some of its early losses, and is now only slightly down – although prices seems pretty volatile. London’s blue-chips are being given a slightly boost by a weaker pound, while NatWest is leading risers.

08:42 AM

Spanish output jumps 16.7pc in third quarter

Pedro Sánchez - Ballesteros/AP

Spain’s economy grew 16.7pc in the third quarter, continuing the trend of record-breaking growth readings we expect to see this morning.

The rebound, which followed 17.8pc fall in second quarter, beat expectations for 13.5pc growth but is likely to be weaker than other major countries given Spain’s reliance on the battered tourism industry.

As with other readings, the figures offer a snapshot of a lost world in which restrictions were being eased and economic activity was rubber-banding back. Now, with tighter restrictions in place and a surge in case numbers, the outlook is much more bleak.

Bloomberg Intelligence’s Maeva Cousin said:

The country’s reliance on tourism, which has been decimated by the pandemic, has proved a major liability in this crisis and will continue to weight on Spain’s prospects until a vaccine is found.

08:28 AM

Big tech round-up

It was a big night for Big Tech, with all of America’s top technology firms except Microsoft issuing results at the same time. Here are our stories:

iPhone sales fall by a fifth after new Apple smartphones delayed: Sales of Apple’s iPhone fell by 21pc in the last three months after the company delayed the release of its latest handsets, although the tech giant’s total sales grew thanks to record revenues from its Mac computers.

The owner of British Airways has sunk to a €6.2bn pre-tax loss loss for the first nine months of the year as the pandemic crushed demand for air travel.

My colleagues report:

IAG made a profit of €2.3bn for the same period last year.

The FTSE 100 group said Covid has had a material impact on the global airline and travel sectors since late February and there were “no immediate signs of recovery”.

Chief executive Luis Gallego said the €1.9bn operating loss including exceptional items relating to fuel hedges and restructuring costs at BA and Aer Lingus.

‘These results demonstrate the negative impact of Covid-19 on our business but they're exacerbated by constantly changing government restrictions,” he said.

After a pause for breath yesterday, European market are once again tumbling today, with the pan-continental Stoxx 600 down 0.8pc as virus fears hit miners and car manufacturers.

If these losses holds, it will make for five days of successive drops.

Bloomberg TV - Bloomberg TV

08:09 AM

France record records third-quarter growth

Macron - REUTERS/Gonzalo Fuentes/Pool

France’s economy grew by a record-breaking 18.2pc in the third quarter, as activity rebounded in the face of widespread stimulus and easing restrictions.

The jump – which marks the first in a string of eurozone GDP figures to be released this morning – is a record for three-month growth, and follows a 13.7pc drop over the previous quarter. It leaves France’s economy 4.3pc smaller than in September 2019.

The figure is something of a false dawn, representing the absolute peak of France’s output recovery, which latest indicators suggest may have lost steam somewhat over recent weeks amid soaring case numbers and new restrictions.

Yesterday, European Central Bank President Christine Lagarde warned the bloc faces a bleak November, and is at risk of slipping back into recession.

ING economist Charlotte de Montpellier said:

French GDP growth figures for the third quarter are like a ray of sunshine that pierces the clouds for a short moment on a rainy autumn day: they remind us nostalgically of the heat of summer, but do not allow us to forget that current realities are much less pleasing. France has entered its second dip and the prospects for a significant recovery in 2021 are darkening sharply.

07:46 AM

NatWest swings to profit but warns of looming challenges

Alison Rose - Dominic Lipinski/PA Wire

NatWest Group swung to a profit in the third quarter after setting aside less cash to deal with virus-induced loan defaults, but warned of “challenging times ahead”.

My colleague Simon Foy reports:

The bank, which remains 62pc state-owned after a £46bn bailout during the 2008 financial crisis, posted a £355m pre-tax profit for the three months to September, beating analyst estimates of a £75m loss.

Last year, the bank made an £8m pre-tax loss for the same period.

Previously known as Royal Bank of Scotland, NatWest factored in a further £254m provision for expected bad loans, compared to its forecast of £628m. Full-year provisions for bad loans would be at the lower end of its £3.5bn to £4.5bn range.

It comes after rivals Lloyds, Barclays and HSBC also set aside less cash for bad loans in their third quarter updates this week compared to earlier in the year.

Good morning. The FTSE 100 is set to open firmly in the red as virus cases continue to surge in the West and investors jitters over next week's US presidential election enveloped markets.

There was also fresh concerns about the outlook for technology giants.

Asian stocks sank on Friday as investors looked ahead to next week's US presidential election and weighed the chances of economic stimulus from Washington and Europe.

Benchmarks in Tokyo, Hong Kong and Seoul all retreated. Shanghai swung between gains and losses.

The Nikkei 225 in Tokyo fell 0.8pc to 23,147.14 and the Hang Seng in Hong Kong lost less than 0.1pc at 24,580.22.

The Shanghai Composite Index was down 0.1pc at 3,269.45 at midday after the ruling Communist Party said it will transform China into a self-reliant "technology power" as a feud with Washington hampers access to high-tech components.

The Kospi in Seoul retreated 1.2pc to 2,298.96 and Sydney's S&P-ASX 200 was 0.3pc lower at 5,945.20.

India's Sensex opened up 0.4pc at 39,906.14. New Zealand, Singapore and Bangkok retreated.

Coming up today

Corporate: Glencore, IAG, NatWest Group (Interim); ConvaTec Group Plc (Trading statement)

Economics: GDP third quarter (eurozone, Germany, France, Italy, Spain), personal income and spending (US)

A horse trainer who was accused of the murder and rape of a showjumper he was in an “illicit relationship” with has been found dead before the second day of his trial was set to begin.

If, as appears more likely than not, Donald Trump returns to the White House come January 20 2025, China will become America’s unmatched foreign policy priority. But the happy days of Trump’s red-carpet fetes in Beijing are long forgotten.

Iran replaced a destroyed radar installation within hours of an Israeli strike on an air base last week in an attempt to make it appear as though the damage had been minimal, it has been claimed.

Hezbollah has launched a series of drone strikes against Israeli military bases, in its deepest attack inside Israel since the start of the war in Gaza.

When you are fighting to stay in the title race and need a win at the home of your city rivals, you cannot get away with the calamitous defending that gifted Everton the lead against Liverpool.

In a suit being brought by her ex-cameraman, Megan Thee Stallion is being sued for allegedly creating a hostile work environment and forcing her former videographer to watch her having lesbian sex.

Last summer there were high expectations that Ukraine’s major counter offensive would succeed in driving Russian forces back, setting the stage for victory. That didn’t happen; instead the offensive faltered and gained little ground. This failure can be laid squarely at the feet of Western refusal to supply adequate military aid. The result was a silent backlash in domestic politics both sides of the Atlantic, which undoubtedly contributed to the US president’s failure to get a further aid packa

"We pulled over and I got out of the car and saw that an alligator had him by the leg," Walter Rudder recalled to a local news outlet about the scary incident

Police say that the youngster discovered a ‘massacre’ at the family home in Oklahoma City and that at least one of the child victims was shot dead in their bed

An Israeli attack on Iranian territory could radically change dynamics and result in there being nothing left of the "Zionist regime", Iran's President Ebrahim Raisi was quoted as saying on Tuesday by the official IRNA news agency. Raisi began a three day visit to Pakistan on Monday and has vowed to boost trade between the neighbouring nations to $10 billion a year. On Friday, explosions were heard over the Iranian city of Isfahan in what sources said was an Israeli attack but Tehran played down the incident and said it had no plans for retaliation.