The MoneySmart Guide to Retirement Part 3: Growing Your Wealth

Money means different things to different people. For some, it’s a new handbag, a bespoke cocktails and ski holidays in Hokkaido.

Call us lazy, but to many of us here at MoneySmart, it means freedom from a life on the hamster wheel.

In this third installment of our 4-part retirement series created in conjunction with CNA (see the first and second parts here), we’ll have a look at how to grow that hard-earned cash into a nice retirement nest egg.

How much do you need to save for retirement?

Surveys published in the local news are always trumpeting the next big sum that Singaporeans think they need to retire, with one previous estimate hovering at over $1.3 million for a retirement income of $3,000 a month.

But you don’t need me to tell you that these things are highly personal. How much you need for retirement depends on factors like your current and desired lifestyle, your retirement age and where you retire.

If you want to retire early, take mini retirements at various points in your life or retire in Thailand, your retirement plan will look quite different from that of the average Singaporean’s.

To estimate how much you need, it’s best to work backwards based on your desired income. Your current spending needs should give you a good starting point. You can then adjust upwards for inflation, healthcare needs, your future insurance premiums and any additional lifestyle perks you wish to enjoy like travel.

Surveys on how much you need to retire tend to add up the total amount to a massive six or seven figure lump sum. But in reality, you’re unlikely to have to amass that amount upfront. Instead, it can be less intimidating to aim for a certain amount of passive income every month.

The multi-layered retirement portfolio

Nobody except Scrooge McDuck keeps a lump sum of cash in a vault to use in retirement and occasionally swim in.

In reality, your retirement portfolio will consist of several layers which together offer you a diversified source of passive income:

Base layer: CPF LIFE

Additional layer: insurance products, i.e. annuities

Additional layer: income-generating investments, e.g. rental, dividends, bonds

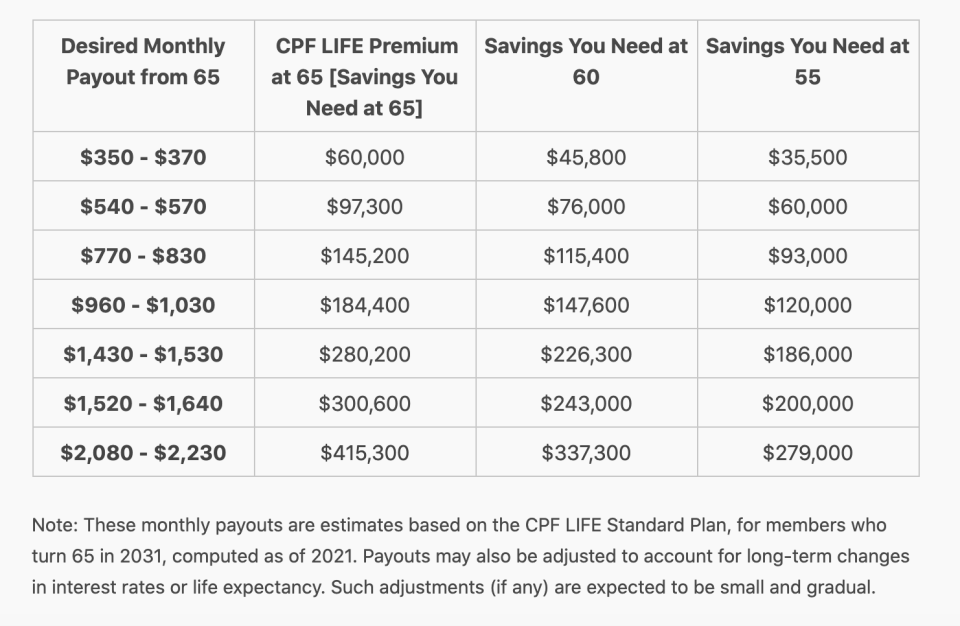

Layer 1: CPF LIFE

The base layer will be your CPF LIFE payouts. Love it or hate it, the CPF system has the advantage of being virtually risk-free. Even if all your other investments tank or run out, you can still fall back on CPF LIFE, which offers payouts for life.

If you’re a Singapore Citizen or Permanent Resident, you are enrolled as a CPF member.

Salaried employees receive CPF contributions every month. These are deducted from your salary and paid into your accounts together with additional sums from your employer, and the total is allocated into your Ordinary Account (OA), Special Account (SA), and MediSave.

When you reach retirement age, CPF merges your OA and SA balances to determine how much you can get in monthly payouts through CPF LIFE. The total savings (OA + SA) tells you how fat you can expect your CPF LIFE paychecks to be.

If you’re aged 55 to 79, you can use the CPF LIFE Estimator to automatically generate your CPF LIFE payout based on your Retirement Account (RA) balance.

Those who are younger can only use the above as a gauge. The numbers will of course rise over the years to account for inflation.

Not satisfied with your CPF balance? You can top up your own SA (if you’re under 55) or RA (for over 55s). Alternatively, if you have other forms of income or retire later, you can delay your CPF LIFE payouts up to age 70. This enables your CPF savings to sit in your RA accruing interest for up to 5 more years.

Layer 2: Insurance products, a.k.a. annuities

Turns out, those insurance agents you’ve been brushing off at the MRT station might actually have something useful to say.

Certain types of insurance products offer a way to accumulate wealth over an extended period of time. You pay money into the plan, wait a certain number of years, and then, upon the plan’s maturity, receive more money than you put in.

Such products include endowment plans and whole life insurance, but for the purpose of retirement, the most relevant type is called the retirement annuity.

This is an insurance policy that will eventually pay out a regular income, usually on a monthly basis. (Fun fact: CPF LIFE is also a type of annuity.)

When choosing an annuity (assuming you’ve decided you want one in your portfolio), it’s best to work backwards by checking with the agent or insurer how much you need to pay in in order to generate $X monthly income upon maturity. These payouts can either be for a fixed term of a number of years or for life.

In order to accrue as much as possible with minimal pain, the best move you can make is to start early. This enables you to minimise your premiums.

You should also look for a premium payment plan that you’re comfortable with — for instance, you might want one with a premium payment term of just 10 to 15 years so you can save assiduously for a short period before sitting back and letting the money grow.

Layer 3: Investment income

The third layer of your retirement portfolio is made up of everything else you could possibly do to generate passive income, including the following:

Renting out property

Dividends from stocks and REITs

Fixed income assets like bonds

We couldn’t possibly cover everything to know about investing here. But if you’d like to start learning, head to our newbie’s guide to investing.

Note that you don’t necessarily need to jump into income-generating investments right away. For instance, you might wish to invest in growth stocks without dividends when you’re younger and have a higher risk tolerance, and then switch to dividend-yielding blue chip stocks later on in life.

Saving up for your retirement magic number

When it comes to retirement planning, the best thing you can do is to start early.

Compounding interest gives early birds a huge advantage. That’s because as your money grows, you earn interest not only on the amount you pumped in, but also on any interest earned up to that point (i.e. interest on interest!). So, your money grows exponentially with time.

Trouble is, lots of people put off investing when they’re younger because they don’t have much cash or don’t know how to invest.

Our advice? If you have youth on your side, don’t wait to start. These days, there are tons of idiot-proof ways to start investing even with small amounts, like robo advisors and regular savings plans.

Finally, the perfect plan for you right now might no longer be perfect as you age. As you move closer to your desired retirement age, you need to lower your risk levels, just in case another pandemic strikes and markets tank just as you’re about to begin your life of leisure.

Tune in to Money Mind every Saturday 10.30pm on CNA, your weekly guide to making the most of your money. Stay ahead of economic, business and investment trends from Asia and beyond. Go to Money Mind for more.

Liked this article? Share it with friends & family.

The post The MoneySmart Guide to Retirement Part 3: Growing Your Wealth appeared first on the MoneySmart blog.

MoneySmart.sg helps you maximize your money. Like us on Facebook to keep up to date with our latest news and articles.

Compare and shop for the best deals on Loans, Insurance and Credit Cards on our site now!

The post The MoneySmart Guide to Retirement Part 3: Growing Your Wealth appeared first on MoneySmart.sg.

Original article: The MoneySmart Guide to Retirement Part 3: Growing Your Wealth.

© 2009-2018 Catapult Ventures Pte Ltd. All rights reserved.