That's all from us for today and indeed this week - thanks for reading. We are back as usual on Monday morning, so do join us then. Have a good weekend.

03:39 PM

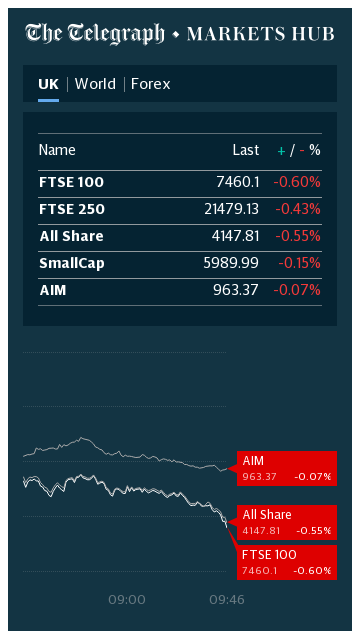

London market jumps

London has ended the week on a high, with the FTSE 100 adding almost 70 points to about 5,852, or 1.1pc higher. The index lost some ground this afternoon however after being up about 1.6pc earlier in the day.

Barclays was the biggest riser, up more than 6pc, with Lloyds Banking Group, HSBC and Standard Chartered also posting respectable gains.

Pearson and InterContinental Hotels too the wooden spoon with falls of almost 2pc.

Across the pond the S&P 500 and the Dow are modestly higher, with investors expecting progress in talks on the next coronavirus aid bill as the presidential election draws ever closer.

The Nasdaq, however, was weighed down by a 10pc slump in chipmaker Intel after it reported a drop in margins as consumers bought cheaper laptops and businesses clamped down on data centre spending.

03:00 PM

Philip Day's Edinburgh Woollen Mill staves off collapse for another 10 days

Edinburgh Woolen Mill

Philip Day’s Edinburgh Woollen Mill has secured another grace period of 10 days before his retail empire falls into administration.

My colleague Laura Onita reports:

The company, which has amassed several fashion chains over the years including Jaeger, Peacocks and Austin Reed, went back to the High Court on Thursday to ask for further protection from creditors such as landlords or suppliers.

That request has now been granted, the company told staff in a memo on Friday.

But if Mr Day, who lives in Switzerland, fails to find a buyer for some of the brands or secure more cash in the coming days, it will be forced to formally appoint administrators at FRP, with more than 21,500 jobs at risk.

“We will use this time as best we can to protect the businesses and save jobs,” staff were told.

“[We] have made good progress, but it is a complex and difficult process. What is clear is that … it will mean a lot of change for all of us and inevitably a significant number of store closures.”

The firm, which was badly hit by the pandemic, has already shut 50 of its 1,100 stores, with another 100 sites earmarked for closure. About 600 Peacocks and Edinburgh Woollen Mill staff have already been made redundant.

02:26 PM

Kudlow: 'Ball not moving much' on stimulus

Larry Kudlow

White House economic director Larry Kudlow said “the ball’s not moving much right now” on negotiations over an additional round of federal stimulus, even as virus cases spike in parts of the US raising the prospect of further shutdowns.

Bloomberg has the details:

“It’s very difficult,” Kudlow said Friday during an interview with Bloomberg Television, adding that there are still a number of issues dividing the White House and Democrats. “The clock is ticking, as you know.”

Kudlow signaled pessimism over the chances of getting a bill before Election Day, saying disagreements remain over policies like liability protection and assistance to undocumented migrants. Even if a deal were reached, Kudlow said, it would be hard to draft and pass in the 11 days before voters head to the polls.

Kudlow said he had heard that “the GOP conference in the Senate would be willing to support a bill as long as it is a genuinely bipartisan deal and their asks are included.” He said he wasn’t aware of Senate Majority Leader Mitch McConnell -- who opposes a larger spending package -- telling the White House not to make a deal.

01:56 PM

Tesla to recall 30,000 cars imported into China

Tesla

Tesla is recalling almost 30,000 Model S and X cars imported into China because of a problem with their suspension.

My colleague Alan Tovey reports:

A recall notice was issued on China’s official market regulation site and affects vehicles built between September 2013 and August 2017.

The vehicles were built in Tesla’s US plants and the problem is described as a weakness in the suspension which can crack after a “large external impact”.

US regulators investigated an alleged defect with the Model S’s suspension in 2016, but decided it was not an issue. Tesla shares were down just under 1pc in early US trading.

01:42 PM

Wall Street opens in the green

US stocks climbed at the open as corporate earnings continue to broadly beat expectations even as rising virus cases threaten the economic recovery.

The tech-focused Nasdaq opened marginally lower.

US market data - Bloomberg

01:07 PM

Handover

Time for me to hand over to my colleague Simon Foy, who will steer the blog into the evening. Thanks for following along today!

01:03 PM

JPMorgan cuts estimate for fourth-quarter UK growth

Economists at JPMorgan have cut their forecast for UK fourth-quarter growth in half in the wake of this morning’s PMI readings, warning a recovery looks past its peak.

Bloomberg reports:

JPMorgan now expects the economy to expand just 2.1pc in the fourth quarter, down from 3.9pc previously. The forecast, which is based on third-quarter growth of 15.9pc, implies no monthly growth in October, November or December.

“The latest mobility data for October show that retail and recreational activity is declining across the country rather than just in the areas with highest restrictions,” Allan Monks, an economist at the firm wrote in a note. “This suggests a broader economic hit via a general confidence channel.”

"How can Q4 show growth if the economy doesn't grow at all during Oct, Nov or Dec?"

Because you compare the average GDP over a quarter with the avg GDP over the previous qtr.

eg. example here 👇

no growth in Oct, Nov, Dec (GDP stuck at Sept level- but still quarterly growth. pic.twitter.com/FytdyPjC3n

The pound has risen in recent minutes after Reuters reported France’s government has told its fishing industry it could get smaller catch from UK waters from 2021.

The news is a signal that Emmanuel Macron may be leaning toward a compromise to help ease a trade deal. Access for UK fisherman, despite the industry representing a tiny proportion of the UK’s economy, has been a key tension in talks.

12:37 PM

Wall Street set to rise

With under an hour until the US open, futures trading is pointing to moderate gains of around 0.3pc on Wall Street’s top indices.

11:55 AM

Travelodge keeps ties with top landlord

Travelodge has convinced its biggest landlord not to abandon the brand and move to a splinter organisation.

My colleague Oliver Gill reports:

Secure Income, a listed property investment trust managed by Nick Leslau, announced it would not exercise a break clause across its 123 Travelodge hotels.

The decision marks a victory for Travelodge, which was at risk of its property owners deserting it to either move to other brands or set up their own chain.

Earlier this year Travelodge was plunged into crisis after having to shut hotels because of coronavirus.

The privately owned group has yet to make a final decision about a CVA, although sources say one is expected in the coming weeks.

Further details about the consequences of a CVA, including numbers of job losses or shop closures, were unclear on Friday…Insiders say Caffe Nero, which is working with KPMG on its options, is expected to seek steep rent cuts from landlords as part of any restructuring deal.

10:47 AM

Huawei reports slowing sales growth

Chinese telecoms giant Huawei endured slowing sales growth during the third quarter of this year amid new US sanctions and “intense pressure” from the coronavirus pandemic.

My colleague Matthew Field reports:

The embattled company said on Friday that its sales growth was up 9.9pc for the first nine months of the year compared to the previous period – down substantially on the 24pc it reported in 2019.

It reported revenues of just over $100bn (£76bn) with a profit margin of 8pc, despite a US blacklisting that has threatened its supply of semiconductor chips.

“As the world grapples with Covid-19, Huawei's global supply chain was put under intense pressure and its production and operations saw increasing difficulties,” the company said.It vowed to “do its best to find solutions, to survive and forge ahead”.

European markets have risen strongly today with the FTSE 100 leading the bank as lenders jump.

10:07 AM

Virgin Holidays commits £203m in refunds

Virgin Holidays has committed to paying out £203m in refunds to customers who had their trips cancelled during the pandemic following an investigation by the competition watchdog.

My colleague Simon Foy reports:

The Competitions and Markets Authority said it had “secured formal commitments” from the company to ensure its customers receive their refunds by Nov 20 at the latest.

If the refunds are not returned within the agreed time frame, the CMA said it was prepared to take the company to court.

The watchdog received hundreds of complaints from people who had not received refunds from Virgin, with some told that they would have to wait as long as four months to get their money back.

Today’s UK flash PMI readings show the recovery has “lost its legs”, says Samuel Tombs from Pantheon Macroeconomics. He writes:

The second wave of Covid-19 is the obvious driver of the slowdown, though the recovery likely would have decelerated anyway, given that the burst of pent-up demand for services after the lockdown was lifted in July never was likely to be sustained.

Note too that the PMI is a diffusion index which does not capture the magnitude of changes in demand at businesses. It will be too upbeat if, as seems to be happening now, most firms are growing modestly but a few in the consumer services sector are experiencing dramatic falls in demand.

Dean Turner, from UBS Wealth Management, adds:

The flash PMIs point to the UK economy posting another month of expansion in October, although momentum is clearly fading. Moreover, fresh challenges still lie ahead, given the renewed social restrictions which are impacting economic activity across the UK and Europe.A common theme amongst this morning's PMIs across Europe is the resilience of manufacturing as compared to services. Given that service industries will feel the greatest burden from new restrictions to stem the spread of Covid-19 infections, this isn’t a great surprise.

However, as services are a higher share of economic activity, the conclusion is that the final quarter of this year will see the pace of growth slow dramatically from the third quarter bounce.

09:34 AM

Money round-up

Here are some of the day’s top stories from the Telegraph Money team:

Why gold has lost its shine, but will sparkle again soon: Gold has been a phenomenal investment this year, protecting savers' nest eggs by making strong returns. But more recently the price has started to decline, leaving owners bemused on whether to stick or switch.

Commenting on those PMI figures, Duncan Brock from the Chartered Institute of Procurement and Supply – which helped gather the data – said:

Fears over inherent weaknesses in the UK economy materialised this month with a sudden fall in the overall index showing a sharp drop in new orders and a continuing erosion of employment opportunities.

Where some businesses were largely unaffected or were able to recoup losses quickly following the worst of the pandemic, consumer-facing businesses were the worst hit and some are now concerned about the prospect of total ruin.

Either unable to fully open or tempt customers through the doors, hospitality firms saw their hands tied by further lockdown restrictions, safety measures for staff and customers, and the public more reluctant to leave their homes

A rising number of manufacturers meanwhile reported that worries over Brexit led to increased stock piling of inputs. One-in-three companies that reported higher input inventories citing Brexit as the cause.

UK figures have come in lower than expected across the board, although all three gauges indicated continued expansion.

Here’s how they came in:

Services: 52.3 (Sep: 56.1)

Manufacturing: 53.3 (Sep: 54.1)

Composite (a weighted balance of the two): 52.9 (Sep: 56.5)

IHS Markit, which gathered the data, said:

UK private sector companies indicated another overall increase in business activity during October, but the rate of expansion slowed considerably since the previous month.

This reflected a much weaker contribution from the service economy, with survey respondents often commenting on tighter restrictions across the hospitality sector and the impact of local lockdowns on general consumer spending.

As a result, service providers reported a decline in new business for the first time since June, which contrasted with another solid expansion in new orders received by manufacturing companies in October.

IHS Markit - IHS Markit

Here are some key points:

Total new business volumes across the UK private sector decreased

October data indicated a steep fall in employment numbers, with another month of deep job cuts signalled in both the manufacturing and service sectors

Business expectations for the next 12 months eased again in October and the degree of confidence was the lowest since May

IHS Markit’s Chris Williamson said:

The pace of UK economic growth slowed in October to the weakest since the recovery from the national COVID-19 lockdown began. Not surprisingly the weakening is most pronounced in the hospitality and transport sectors, as firms reported falling demand due to renewed lockdown measures and customers being deterred by worries over rising case numbers.

The slowdown would have been even more pronounced had it not been for exports rising as overseas customers sought to secure orders before potential supply disruptions as Brexit draws closer

08:28 AM

UK PMIs coming up

The UK’s flash PMIs are coming up shortly. Britain has been behind Europe in slowing down, with economists expecting continued activity improvements this month.

Here are the predictions, which indicate continued expansion at a solid pace:

Services: 53.9 (Sep: 56.1)

Manufacturing: 53.1 (Sep: 54.1)

Composite (a weighted balance of the two): 54 (Sep: 56.5)

08:20 AM

Eurozone PMIs reaction: Services slide set to continue

The divergent performance we’ve seen in today’s eurozone PMI figures is set to extend into winter, economists say.

Nicola Nobile from consultancy Oxford Economics says:

Activity in the services sector contracted strongly, continuing with a trend that started after the summer. This is likely due to the worsening of the health situation and the reimposition of containment measures. This dynamic will very likely continue in the coming months, given the sharp rise in cases across Europe over the last few weeks.

A growing divergence is evident between a stronger #manufacturing recovery and a deepening downturn in eurozone services, the latter hit by rising COVID-19 restrictions pic.twitter.com/MN5Jvkg1dO

Bert Colijn, from Dutch lender ING, says the readings indicate the eurozone economy is re-entering contraction territory:

The difference between services and manufacturing performance at the moment makes sense. The most restrictive measures taken so far have hit the recreational sector more than other parts of the economy. That impacts the service sector disproportionally. The same holds true for the change in behaviour among the population, as services require more in person interaction and rely more on personal consumption.

From here on, the path for the economy is highly uncertain. With cases continuing to rise at a worrying pace, more restrictive measures in the eurozone definitely cannot be ruled out. Today’s PMI confirms that after a stellar third quarter GDP figure, we could be in for the dreaded double dip.

Daniel Bergvall from Swedish bank SEB says it’s time to buckle up for a tough fourth quarter:

One conclusion from today’s number is that lockdown measures are aimed at minimising social interaction by reducing the scope for social activities while at the same time keeping a large part of the economy open. That will keep manufacturing going and lessen the negative effect on the overall economy. Still, PMI and other data clearly point towards a weaker Q4 that we previously have expected.

08:06 AM

Eurozone PMIs show manufacturing/services divergence

Eurozone PMIs are in, and they confirm the trend we’ve already seen this morning of divergent performances for the manufacturing and services sectors.

Here are its readings (where a score beneath 50 indicates contraction):

Services: 46.2 (Sep: 48)

Manufacturing: 54.4 (Sep: 53.7)

Composite (a weighted balance of the two): 49.4 (Sep: 50.4)

IHS Markit, which gathered the data, said:

Business activity fell back into decline across the eurozone in October as accelerating growth of manufacturing output was overwhelmed by a steepening deterioration in the service sector amid rising Covid-19 worries. Germany was the only bright spot, as France and the rest of the region as a whole fell deeper into decline.

Here are some key findings:

The rate of job losses eased, but forward -looking indicators deteriorated

Employment was cut across the eurozone as a whole for an eighth successive month

The ongoing need to cut employment was in part linked to companies reporting excess capacity, as indicated by a further reduction in backlogs of work

Deflationary pressures moderated during October

Signs of underlying price pressures building were evident via the largest rise in input costs since February

IHS Markit’s chief business economist Chris Williamson said:

The survey revealed a tale of two economies, with manufacturers enjoying the fastest growth since early-2018 as orders surged higher amid rising global demand, but intensifying COVID-19 restrictions took an increasing toll on the services sector, led by weakening demand in the hard-hit hospitality industry.

07:54 AM

European market rise after Barclays results

Barclays’ strong results have sparked a rally for lenders, lifting market across Europe.

US private equity fund Lone Star has swooped on retirement housebuilder McCarthy & Stone with a £630m bid, as it seeks to gain exposure to the retirement living market.

My colleague Simon Foy reports:

The fund has offered investors in the Bournemouth-based company 115p per share, representing a 39pc premium to their closing price on Thursday.

Shares soared by more than two-fifths to 118p in early trading. The stock had fallen 44pc this year prior to the bid.

Paul Lester, McCarthy & Stone's chairman, said the all-cash offer "represents a compelling and attractive opportunity for shareholders to realise and crystallise their investment".

He added that the bid “provides a meaningful premium to the prevailing share price notwithstanding the backdrop of the wider risks posed by the political and macro-economic environment”.

Services nerves have also spread to Germany, but the manufacturing sector of Europe’s biggest economy continued a strong recovery, beating expectations to keep its overall growth rate steady.

Here are its readings (where a score beneath 50 indicates contraction):

Services: 48.9 (Sep: 50.6)

Manufacturing: 58 (Sep: 56.4)

Composite (a weighted balance of the two): 54.5 (Sep: 54.7)

IHS Markit, which gathered the data, said:

A further rise in manufacturing output helped to support growth across the German private sector in October, latest PM showed. However, in a sign of a two-speed economy emerging, service providers recorded a modest decline in activity amid new restrictions and heightened uncertainty due to a second wave of coronavirus cases.

IHS Markit - IHS Markit

Here are some key points from its findings:

Service providers reported an impact on demand from new restrictions and increased uncertainty associated with a rise in the number of Covid-19 cases

In manufacturing, latest data showed a record increase in order book volumes

On the employment front, however, it was a case of roles reversed, with the service sector seeing a fourth straight monthly rise in payroll numbers, while manufacturers recorded further staff cuts

Latest data showed a rise in average charges for goods and services for the first time since February

October’s survey showed a weakening of expectations for the first time in seven months

IHS Markit’s Phil Smith said:

Encouragingly, the German economy is showing a degree of resilience in the face of a second wave of coronavirus cases, October’s flash PMI data suggests.

While some services firms in Germany have been hit by new restrictions and increased uncertainty around a ‘second wave’, the decline in service sector activity has so far been quite limited, whilst at the same time the country’s economic performance is being buoyed by a strong showing from manufacturing.

Data for the whole Eurozone comes out at 9am.

07:23 AM

French slowdown deepens

A slowdown in France’s services sector intensified this month, with activity continuing to edge lower amid heightening restrictions.

‘Flash’ purchasing managers’ index figures for the country show continued minor growth in its manufacturing sector couldn’t offset an overall service-driven decline. The slowdown was faster than expected.

Here are its readings (where a score beneath 50 indicates contraction):

Services: 46.5 (Sep: 47.5)

Manufacturing: 51 (Sep: 51)

Composite (a weighted balance of the two): 47.3 (Sep: 48.5)

IHS Markit, which gathered the data, said:

The further contraction in aggregate business activity came amid a marked deterioration in demand.

New orders fell for the second month running and at the quickest pace since May. Similar to the trend for output, service providers posted a sharp reduction in new work, while goods producers registered marginal growth for the third month in a row.

Anecdotal evidence indicated that the service sector downturn was predominantly driven by the recent surge in Covid-19 cases.

IHS Markit - IHS Markit

Here are some key findings:

Export orders received by French private sector firms continued to fall at the start of the fourth quarter

In line with softer demand conditions, private sector companies continued to cut their staff numbers

Backlogs of work at French businesses fell for the third month in a row

On the cost front, input prices continued to rise

Despite facing higher input costs, private sector firms opted to continue cutting their average output prices

IHS Markit economist Eliot Kerr said:

The latest release of PMI data delivers more disappointing news for French businesses. The results suggest that the recent rise in Covid-19 cases and subsequent tightening of restrictions has had a notable negative impact on business conditions.

Germany’s PMI data is next, at half past.

07:13 AM

FTSE 100 rises

The FTSE has risen 0.4pc shortly after the open, outperforming a mixed open across Europe. Barclays shares are up about 3.5pc currently following its strong results.

Bloomberg TV - Bloomberg TV

07:11 AM

Britain signs trade deal with Japan

Earlier this morning, Britain officially signed a trade deal with Japan, its 18th-biggest trading partner.

The Department for International Trade estimates the trade deal with Japan will add 0.07pc to UK GDP over the “long term”.

The agreement also has a much wider strategic significance. It opens a clear pathway to membership of the Comprehensive Trans-Pacific Partnership – which will open new opportunities for British business and boost our economic security – and strengthens ties with a like-minded democracy, key ally and major investor in Britain.

Our historic UK-Japan trade deal will:

✅ Bring jobs & growth to industries across the UK 🇬🇧, from farming to tech

✅ Draw two democratic island nations closer together

✅ Pave the way for us to join the Trans Pacific Partnership

London Stock Exchange group met analyst expectations with slightly lower third-quarter revenues of £524m.

The bourse operator said it had shown a “resilient” performance over the three months to the end of September, despite “challenging market conditions”.

It said it was making “good progress” on its planned acquisition of financial data giant Refinitiv as part of a strategy to diversify into the lucrative data sector.

Referring to its agreement to sell Italy’s stock exchange to rival Euronext as part of efforts to get the refinitiv deal past regulators, LSE group added: “we believe the proposed divestment of the Borsa Italiana group will significantly contribute to addressing EC concerns”.

Chief executive David Schwimmer said:

We remain focused on our strong operational resilience, continuity of services to our customers and market participants, and the wellbeing of our employees, the majority of whom continue to work remotely.

06:55 AM

Retail sales reaction: Probably the peak

Responding to this morning’s retail sales data, Samuel Tombs from Pantheon Macroeconomics says September is “probably this year’s peak” given falling incomes and further lockdowns. he adds:

Looking ahead, households will continue to spend a larger-than-usual fraction of their incomes on goods. The second wave of Covid-19 will prompt more people to spend less on services, while food sales will benefit from a decline in eating out and perhaps some renewed stockpiling.

High housing transactions in Q3 and Q4 also will create a strong pipeline of demand for household goods. Nonetheless, households’ disposable incomes will fall over the winter.

Two 👍 observations from Julian. A word of caution on the V. RS are benefitting from “diverted spending” away from restricted sectors (travel & hospitality). Normally RS a good bellwether of economic health - this time RS growth may slow as economy reopens & spending reverts https://t.co/c4fDIHEWo8

James Smith from ING agrees that retail’s “remarkable recovery” is now likely to stall:

While sales increased by another healthy 1.5pc over September, the latest readings from the ONS business impact survey (a wide-ranging questionnaire on the impact of Covid-19) suggests that retailers are beginning to see their turnover level-off – and the latest round of government restrictions will add further pressure.

06:47 AM

FTSE set for small gains

With just over ten minutes until the cash open in London, futures trading is pointing toward minor gains for the FTSE 100, amid a slight continued dip in the pound. European shares are set to open slightly lower.

06:46 AM

Barclays results beat expectations as trading soars

Barclays - Jason Alden/Bloomberg

Barclays bank reported another strong quarter for its traders as market volatility remained high.

The lender’s total trading income jumped 29pc, beating the average 21pc rise across its Wall Street rivals. Securities trading climbed 23pc, while equity trading income was up 40pc.

Chief executive Jes Staley said the group had performed solidly, “with strong income performance in our [corporate and investment bank] more than offsetting headwinds in our consumer businesses.”

In media interview this morning, Mr Staley has said Barclays is prepared for the introduction of negative interest rates, which are currently being mooted by the Bank of England.

The FTSE 100 group registered a £608m charge in preparation for losses on bad loans, beneath the £1bn analysts has expected. It said:

Provided macroeconomic assumptions remain consistent with expectations, we expect the H220 impairment charge to be materially below that of H120 and it is likely that the full year 2021 impairment charge will be below that of 2020

A rise in mortgage demand boosted domestic operations, with Barclays UK returning to a £196m pretax profit after a second-quarter loss:

Barclays said it faces some headwinds in the 2021, including the persistent “low interest rate environment”.

It teased the potential return of shareholder payouts, saying:

The Board recognises the importance of capital returns to shareholders and will provide an update on its policy and dividends at FY20 results

Citi’s Andrew Coombs said the results were a “strong beat” in several areas, anticipating “low single-digit upgrades to 2021 revenues”.

06:24 AM

Clothing sales lag as most non-food stores recover

Non-food stores finally completed a recovery to pre-pandemic sales volume levels in September, 1.7pc above February levels.

Although department store sales are also still slightly shy of a full recovery, it’s clothing stores that once again are suffering the most – sales are still nearly 13pc below February levels.

06:15 AM

Online sales still elevated

Overall, 27pc of the total retail spend in the UK was via online channels last week, with the level remaining elevated compared to before the pandemic but below the peak at the start of lockdown.

06:09 AM

Sales extend gain on pre-pandemic levels

September’s rise puts sales further ahead of pre-pandemic levels, with a true ‘V-shaped’ current present in the figures:

06:06 AM

How sales have shifted

Those figures represent a big beat. Here’s how retail sales have changed over recent years:

06:01 AM

Retail sales smash expectations

Retail sales have come in far stronger than expected. Here are the figures:

Retail sales ex. auto fuel month-on-month: 1.6pc

Retail sales ex. auto fuel year-on-year: 6.4pc

Retail sales inc. auto fuel month-on-month: 1.5pc

Retail sales inc. auto fuel year-on-year: 4.7pc

05:57 AM

KFC to add 5,400 jobs in UK and Ireland – Reuters

KFC - Alex Pantling/Getty Images

Fried chicken chain KFC plans to hire 5,400 new jobs across its 965 restaurants in the UK and Ireland by the end of the year, Reuters reports.

Hospitality has been one of the worst-affected sectors, forcing finance minister Rishi Sunak to offer it more help on Thursday to try to save jobs.

But despite huge swathes of Britain facing local lockdown restrictions, KFC said on Friday it planned to hire 5,400 new staff over the next 2-1/2 months.

The new jobs would be partly supported by the government’s Kickstart scheme, which helps employers create opportunities for 16 to 24 year olds at risk from long-term unemployment, KFC said.

05:54 AM

Retail sales: What the experts expect

Here are the figures economists are predicting from today’s retail sales release (per Bloomberg polling):

Retail sales ex. auto fuel month-on-month: 0.5pc

Retail sales ex. auto fuel year-on-year: 5pc

Retail sales inc. auto fuel month-on-month: 0.2pc

Retail sales inc. auto fuel year-on-year: 3.7pc

05:51 AM

Consumer confidence drop for first time since height of lockdown

UK consumer confidence dropped for the first time since April amid greater worries about personal finances and the wider health of the economy.

Household optimism fell more than expected, from a reading of –25 to –31, according to the latest data from research firm GfK.

All the gauge’s five sub-indices fell, with a willingness to make major purchases at its lowest level since the spring. GfK said much of the data was collected ahead of the latest lockdowns, so the measure is expected to drop further next month.

GfK director Joe Staton said:

Despite low inflation and rock-bottom interest rates, a buoyant housing market and a raft of government financial stimulus measures, the prospect of rising unemployment is severely depressing our outlook

05:43 AM

Agenda: Retail sales could be last hurrah for summer economy

Good morning. It’s set to be a fairly busy end to the week, with UK retail sales data for September set for release at 7am, followed by flash PMIs for October coming out across the morning.

The retail data is expected to be something of a last hurrah for the summer economy, when customers were still being encouraged to head out and spend. If things have gone into reverse since then, the PMIs later on should be one of the earliest indicators of a slowdown.

On the corporate front, results for Barclays will kick off earnings season for London’s top listed lenders.

4) KPMG mulls sale of restructuring division: The potential sale is the latest attempt by a Big Four accountant to reshape their business in face of regulatory and economic pressure.

Global stocks barely budged on Friday as investors tightened positions with less than two weeks to go before the US presidential election and awaited a breakthrough in stimulus talks in Washington.

The final debate between US President Donald Trump and his Democrat challenger Joe Biden presented few surprises for election watchers but slightly reinforced investor caution heading into the November 3 poll.

US S&P 500 futures had dipped slightly after the debate but were mostly flat by midday trade. The underlying index had gained about 0.5pc in the previous day on hopes that the US Congress and the White House could soon strike a deal on another round of Covid-19 stimulus.

Shares in Asia hardly budged, with MSCI’s broadest index of Asia-Pacific shares outside Japan flat while Japan's Nikkei ticked up 0.2pc.

The CSI300 index of mainland China also edged up 0.2pc.

The wife of tech billionaire Forrest Li is set to acquire a mansion in one of Singapore’s most coveted residential areas, even as the luxury property market remains in a lull.

At least two people were killed in a road traffic accident involving multiple vehicles at the junction of Tampines Avenue 1 and Tampines Avenue 4. Read on.

As Leicester City close in on an immediate return to the Premier League, the uncomfortable question looms large: is this the end of the fairy tale for Jamie Vardy?

After veteran Hollywood producer Carol Baum mocked the blonde over her looks and acting ability, Sydney Sweeney has jokingly apologised for having a “great” cleavage and “correct opinions”.

The #Fitspo series is dedicated to inspirational men and women in Singapore leading healthy and active lifestyles. This week: Charge SG founder Vanessa Oh.

Hezbollah has launched a series of drone strikes against Israeli military bases, in its deepest attack inside Israel since the start of the war in Gaza.

Two Malaysian military helicopters collided midair and crashed during a training session on Tuesday, killing all 10 people on board and injuring a swimmer in a pool, authorities said. The helicopters were rehearsing at a naval base in northern Perak state for the navy’s 90th anniversary celebration when the accident occurred, the navy said in a brief statement. A video circulating on social media purported to be of the incident shows several helicopters flying low in a formation.

Before we find fault with Manchester United after reaching the FA Cup final, and there is plenty of it to go around, it is worth considering what would constitute an appropriate response to winning a penalty shoot-out in a match they had deserved to lose?

Victor J. Blue/ReutersOpening statements had not yet begun on Monday when former President Donald Trump dozed off for the first time.He quickly opened his eyes when defense attorney Todd Blanche slid him a note, as prosecutors prepared to kick off opening arguments in the historic trial, which hinges on accusations that the former president falsified business records over a $130,000 hush-money payment to porn star Stormy Daniels in an effort to keep her quiet as the 2016 presidential election lo

With these four blue-chip stocks hovering at a year-low, investors could be looking at potential bargains. The post Share Prices of These 4 Singapore Blue-Chip Stocks Are at 52-Week Lows: Can They Recover? appeared first on The Smart Investor.

When Manchester United won the penalty shoot-out, after extra-time in this stunning FA Cup semi-final, Antony turned and cupped his ears to goad the Coventry City players left desolate on the half-way line at Wembley.

One day apparently in early April, a Russian T-72 tank rolled into battle near Terny, in eastern Ukraine’s Donetsk Oblast. The tank ran over some barbed wire, which fouled its tracks. Out of control, the tank collided with a BMP fighting vehicle.