Retirement Planning In Singapore: 3 Lesser-Known Facts About CPF LIFE

For most Singaporeans, retirement planning involves taking the CPF Lifelong Income For The Elderly (CPF LIFE) scheme into account. CPF LIFE is a life annuity scheme which provides Singapore Citizens and Permanent Residents with a monthly payout for as long as they live.

Payouts for CPF LIFE start from age 65, though members can opt to delay the payouts up to the age of 70 if they do not need the money so soon. For each year that they defer receiving payouts, their monthly payout amount will increase by up to 7%.

In total, there are three CPF LIFE plans that members can choose from. They are the Standard Plan, Basic Plan and the new Escalating Plan.

While the choice of CPF LIFE plan and year to start payouts are common decisions that people usually think about, they are not the only things about CPF LIFE that members need to be aware of.

In this article, we will focus on three important CPF LIFE-related matters that not everyone knows about. While these are lesser known, they are by no means unimportant, especially when it comes to your retirement planning.

# 1 Do You Need At Least $60,000 In Your Retirement Account To Qualify For CPF LIFE?

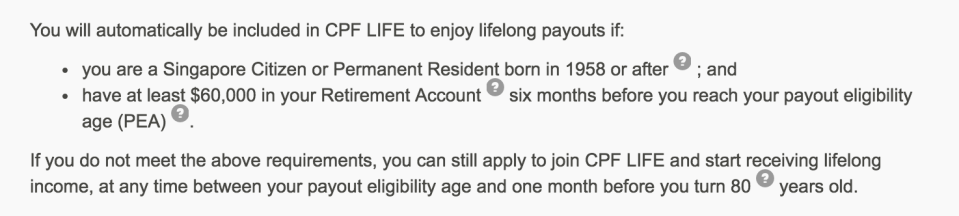

There are two major misconceptions that CPF members often have regarding eligibility for CPF LIFE.

The first is the misconception that CPF LIFE automatically applies to all Singaporeans. This is incorrect. CPF members are included into CPF LIFE only if they are born in 1958 or after* and have at least $60,000 in their Retirement Account (RA) six months before they reach their payout eligibility age (i.e. age, 65).

The second misconception is that CPF members must first have $60,000 in the RA six months before they reach 65 to qualify to qualify for CPF LIFE. However, this isn’t true either.

Source: CPF

The CPF Board has stated that members who do not meet these requirements can still apply to join CPF LIFE and start receiving lifelong income, at any time between their payout eligibility age and one month before they turn 80 years old.

What this means is that even members who do not have $60,000 in their RA can still apply to be part of CPF LIFE.

*If you turned 55 between 1 Jan 2013 and 30 April 2016, you will also be enrolled in CPF LIFE if you have at least $40,000 in your RA when you reach 55 years old.

Read Also: Standard Or Basic Plan? What You Need To Understand About CPF LIFE Plans Before Deciding

# 2 Selling Your Home After 55

At age 55, every CPF member will have a Retirement Account (RA) created for them. Monies from their CPF Special Account (CPFSA) will be used to top up the RA for them, up to the Full Retirement Sum (FRS), which is $171,000 as of 1 January 2018.

If there are insufficient monies in their CPFSA, their CPF Ordinary Account (CPFOA) monies will then be used. CPF members can also opt to set aside the Basic Retirement Sum instead, which is half the amount of the FRS, by pledging their property.

If you do not have this amount set aside, it is okay and no further actions are required on your part. You are not required to make any top ups with cash.

However, if you do sell your property, any CPF refunds paid to your CPFOA from the sale of your property will first go into your RA first. This is as opposed to the monies being returned to your OA, which is what happens if you sell your home before you turn 55.

The misconception here is that all CPF members age 55 and above will need to ensure they hit their FRS, before they are allowed to spend the remaining proceeds on a new home. This is incorrect. CPF members only need to refund the amount which they have used from their CPF to pay for their home and any interest it would have earned.

For example, if your home was paid for using only cash, then you would not need to do any CPF refunds since you did not use any CPF monies to pay for your home in the first place.

Read Also: What Happens To Your Money After You Sell Your Flat In Singapore

# 3 What Happens To Your CPF LIFE Monies After You Pass On?

Some people are worried about what happens to their remaining CPF LIFE monies should they pass on early.

For example, a person at the age of 65 today with $171,000 in their RA will receive about $1,001 a month under the CPF LIFE Standard plan for the rest of their life. If the person lives till age 95, they would have received a total of $360,360 in total lifetime payouts. This is great and one of the best features of CPF LIFE – you don’t have to worry if you out live your retirement payouts.

But what happens if an individual were to pass on just one year later at the age of 66?

In this case, there will be a bequest which will be given out in cash. Let’s see much will this be:

According to the CPF LIFE benefit illustration, a bequest amount of about $158,983 will be given. When you do the math, this is about $12,000 less than the amount the individual has in his RA a year ago, which was $171,000.

This difference of about $12,000 is identical to how much the individual would have received in CPF LIFE payout over the past 12 months. Hence, if you ignore opportunity cost, an individual who passes on early does not “lose out” as the unused monies in his RA is simply returned to his surviving family members.

The CPF website also confirms this.

Source: CPF

This knowledge should alleviate the fear of any CPF members who may, for any reason, worry that they will lose out if they pass on early of the unused portion in their RA.

The post Retirement Planning In Singapore: 3 Lesser-Known Facts About CPF LIFE appeared first on DollarsAndSense.sg.