SI Research: An Interview With Sasseur REIT

Fueling China’s transition from an export-led economy to one driven by domestic consumption is none other than the free-spending younger generation of Chinese consumers that are growing in size.

With rising income, China’s middle-class is growing at an unprecedented pace even beyond the largest cities. The contemporary Chinese consumers are no longer just buying to meet their daily needs. In a big part, higher education has also shaped the way how today’s Chinese consumers spend. With a literacy rate of 96 percent, Chinese consumers have grown highly sophisticated and rising demand for luxurious products have become a way of life.

Riding on this tailwind is Sasseur Real Estate Investment Trust (REIT), the first premium outlet mall REIT listed in Asia on the mainboard of the Singapore Exchange. Listed in March 2018, Sasseur REIT has been generating waves with a slew of positive news.

For one, Sasseur REIT’s most matured Chongqing outlet mall recently smashed records during its 10th-year anniversary sales season. During the 16-day anniversary sale, total sales achieved was a whooping Rmb325 million. On a cumulative basis, average daily sales were up by about 27.6 percent compared to same period last year. First day sales alone, the Chonqing outlet mall reached a staggering Rmb130 million, beating last year sales of Rmb90 million and marking a new one-day sales record for outlet malls in China!

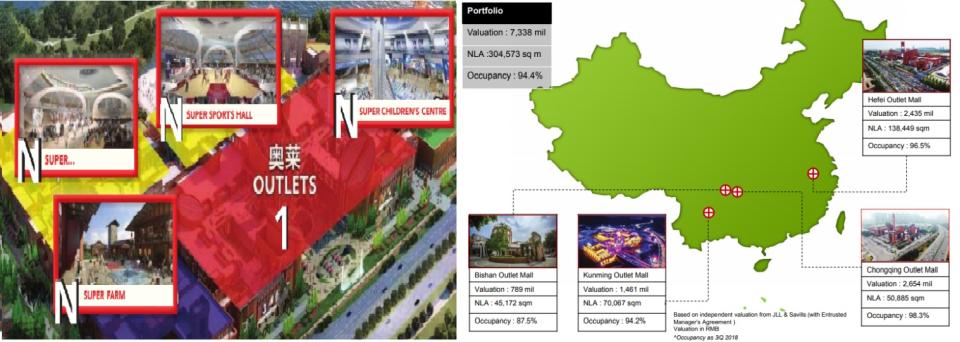

Having demonstrated its growth potential, Sasseur REIT clinched the “Most Promising REIT in Asia” award at the Fortune Times REITs Pinnacle Award 2018. Hearing that Chairman of Sasseur Group Xu Rongcan is in town, Shares Investment took the opportunity to interview Mr. Xu in order to understand about the investment merits of Sasseur REIT. Currently, Sasseur REIT has an initial portfolio of four outlet malls in Chongqing, Bishan, Hefei and Kunming.

Secular Industry Tailwind

Starting with the macro-fundamentals, everyone well knows that domestic consumption is set to spur China’s growth story in the coming decades. How significant is this phenomenon?

According to an independent study by China Insights Consultancy, the nominal Gross Domestic Product (GDP) per capita is projected to grow by a compounded annual growth rate (CAGR) of 7.4 percent from 2016 to 2021, from Rmb54,000 to an estimated Rmb78,000.

In the same period, urban household-consumption expenditure per capita would see 6.7 percent growth to Rmb50,000 in tier-1 cities and 8.2 percent to Rmb39,000 in tier-2 cities. In other words, with all the increase in wealth, China is bound to see a dramatic shift in expenditure towards luxury goods.

By 2021, online platforms would still take up the lion’s share of the expected total retail sales in China, but the outlet industry would be growing at a much faster pace. While outlet malls would be growing by CAGR 24.2 percent to Rmb145 billion by 2021, retail sales in China as a whole is projected to only grow at CAGR of 17 percent.

Partly, the reason behind China’s outlet industry having the strongest growth prospect is due to its nascency. Still at a low base, outlet sales in 2016 was only Rmb49 billion, with an unmet demand of Rmb31 billion. That means that supply has fallen short of the addressable market size for the outlet industry which was estimated to be Rmb80 billion in 2016.

Another reason why the outlet mall industry in China has potential for rapid growth is due to the obvious undersupply of outlet malls compared to other developed countries. According to industry reports, the concentration of outlet mall per gross floor area per 100 residents in China only measured about 0.4 square meter (sqm), compared to 2.4sqm in the US. As the Chinese middle-class continue to grow numbers along with rising disposable income, China’s outlet mall industry is set to overtake the US with total sales of Rmb640 billion – the largest in the world by 2030.

A Class Of Its Own

While classified as a retail REIT, Sasseur REIT’s asset portfolio comprises of outlet malls that could be sub-categorized to an entirely different asset class of its own.

For one, outlet malls are unlike conventional commercial shopping malls. They provide avenues for full-priced traditional retailers to clear merchandises at deep discounted prices (similar to Singapore’s factory outlets at Changi City Point) all through the year, giving good value for money to Chinese consumers. Such goods sold at outlet malls are typically out-of-season products that turnover very quickly in the street of high fashion. Given the deep discounted prices of goods offered at outlet malls, e-commerce platforms do not possess any pricing advantages. On the other hand, outlet malls value-adds consumers by providing an avenue for experiencing products’ quality and ensuring their authenticity.

Due to this nature, outlet malls exhibit consistent counter-cyclical behaviour. For example in the US, one of the largest full-priced retailers Macy saw sales revenue drop from US$26.3 billion in 2007 to US$24.9 billion in 2008, while Tanger – an outlet operator – continued to see sales revenue grow from US$229 million to US$245 million during the same period.

Meanwhile, while investors are increasingly concerned about the ongoing US-China trade war, Sasseur REIT’s management reiterated that its business exposure is to the domestic middle class. In fact, Sasseur REIT’s management is confident that the Chinese outlet industry is set for tremendous growth in the next decade, sharing that Chinese consumers tend to look for value-for-money during uncertainties. This is notwithstanding the Chinese government’s impetus to promote domestic consumption to stimulate the economy, seen from recent moves such as a modest cut in individual taxes and further pledges to reduce import tariffs.

Sasseur’s Unique DNA

While rising consumption expenditure is bound to lift China’s retailing industry, not all segments of retail are bound to benefit from this trend. Conventional shopping malls for example are not shielded from the threat of e-commerce platforms that adds value to Chinese consumers through better conveniences.

In addition, other conventional outlet malls in China, have also become highly commoditised – a global phenomenon that is prevalent in Singapore. This lack of vibrancy in Chinese shopping culture led Sasseur REIT to rethink how it should design and operate its outlet malls.

Pioneering its proprietary Super “1+N” model, Chairman Xu explained that Sasseur REIT’s aim is to create an all-new integrated lifestyle (N) and retail platform (1) centred around the outlet malls to create what they dubbed as Super Outlets. Apart from just shopping, customers can partake in various activities such as sports or experience rural living in its outlet complex. Kids also have their own dedicated section to engage in play and enrichment programmes.

Along with the government’s push to promote Chinese characteristics in its society, Mr. Xu also hopes to capture and enrich the collective experience of its shoppers through Sasseur REIT’s outlet malls. Reminiscing his time as an artist, Mr. Xu also reiterated that artistic and cultural elements also form a big intangible part of Sasseur REIT’s DNA.

In a way, this helped us see why the REIT targets tier-2 cities. Apart from a faster-growing middle class population with greater ability for discretionary spending, Sasseur REIT’s concept of community living, complemented with shopping, is targeted at local residents which form 90 percent of return shoppers. Apart from that, land prices in tier-2 cities are cheaper compared to tier-1 cities, and are also less saturated and less competitive. Overall, the strategy helped Sasseur REIT to enhance foot traffic, shoppers’ time spent and hence retail spending in its outlet malls.

A Symbiotic Business Model

To align tenant-manager performance, Sasseur REIT undertook an entrusted management agreement (EMA) with its sponsor. Under the EMA agreement, the REIT’s income consists of a fixed component with a built-in escalation of three percent per annum, and a variable component which is pegged to a percentage of total tenant sales of each property and let the REIT investors participate the upside of the fast growth in tenant sales. This symbiotic relationship to drive sales allows the REIT-holders to leverage on the outlet malls’ success while the fixed component provides a downside protection.

Some investors have raised concerns about the “short” weighted average lease expiry of 1.3 years based on gross revenue. To that, management explained that due to the fast-growing outlet industry in China, its sales-based leases are short as under-performing tenants can be quickly replaced with better-performing ones. According to the sponsor, this model should benefit both tenants and manager as the group has achieved a CAGR of 40 percent in sales growth over the past 29 years.

Beating Forecasts And Undemanding Valuations

Under the EMA, the sponsor guaranteed, at portfolio level, to cover the shortfall in income should the REIT’s resultant rent fail to meet its targets and the guarantee only falls away after the actual resultant rent has been higher than the guarantee level for two consecutive years. However, thus far, Sasseur REIT has been beating its forecasts without having the sponsor to step in.

In its latest earnings release on 12 November 2018, Sasseur REIT reported 3Q18 EMA rental income of $29.1 million, 0.7 percent higher than the $28.9 million forecast. Meanwhile, distributable income to unitholders at $18.2 million was 4.5 percent higher than forecasted. Overall, 3Q18 distribution per unit (DPU) of $0.01542 was also 4.5 percent higher.

Total sales wise, the four outlet malls posted Rmb2 billion in 3Q18, surpassing forecast by 7.9 percent and growing astonishing 35.7 percent compared to the same period last year.

A distribution yield in FY18 was initially projected at 7.5 percent, based on IPO price of $0.80. This works out to a DPU of $0.06. Considering that the current share price has fallen to $0.69 and that the REIT has beaten its forecast, the actual yield investors are looking at is probably above 8.7 percent.

Furthermore, at the current share price, Sasseur REIT is changing hands at a discount to its book value of $0.771 per share, translating to an 11.8 percent discount to the book value to provide investors with even more margin of safety.

Drawing Large Cornerstone Investors

Going forward, Sasseur REIT has a strong pipeline of potential properties available for acquisition. With two Rights of First Refusal (RoFR) properties in Xi’an and Guiyang and three pipeline properties in Nanjing, Hang Zhou and Changchun, Sasseur REIT could grow its aggregate GFA more than three times, assuming all properties are acquired in the future. Furthermore, the sponsor has intimated that it is actively exploring and expanding its outlet malls that could be added to the supply pipeline in the future.

For retail investors, the best testament to Sasseur REIT’s growth prospects could be none other than the number of cornerstone investors taking part in the REIT’s success. Amongst them are Chinese e-commerce giant JD.com, Bangkok Life Assurance, CKK Holdings and DBS Bank.