What's the next step for HDB owners?

Since the implementation of the total debt servicing ratio (TDSR) framework in 2Q2013, resale prices of HDB homes had declined 10% as at 1Q2016, according to the HDB Resale Price Index. Although prices have fallen, the current market conditions appeal to HDB homeowners who have met the minimum occupation period and are looking to buy a private home. This is because the current prices of HDB flats are still higher than what they were five years ago. Based on the index, homeowners who bought units in 2Q2011 in the resale market would enjoy a capital value return of 3.3% if they were to sell now. In other words, as long as the homeowners are qualified to sell their homes, they should at least break even, without accounting for renovation and transaction costs.

For this group of buyers, more options are available to them. First, prices of both private and public homes have become more affordable. Second, there are more choices available to them, especially with the monthly income ceiling for executive condominiums (ECs) increasing to $14,000 from $12,000 with effect from August 2015.

As prices of HDB flats have become more affordable for owners who have met the MOP, the resale market also saw a pickup in activity, as the number of resale applications rose to 19,306 from 18,100. That is despite greater economic uncertainty as a result of external events. Still, the trade-offs among various options and the deluge of information for HDB homeowners may be overwhelming.

Options for homeowners who bought their flat directly from HDB

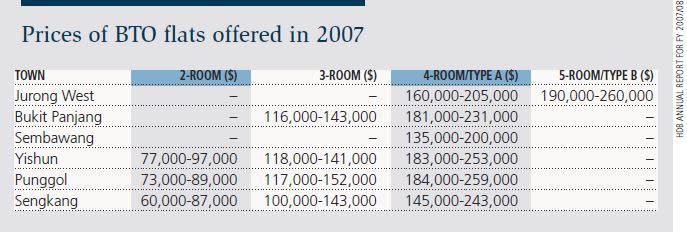

We will first cover the options for homeowners who bought directly from HDB and are qualified to sell their homes in the resale market in 2016. To meet the MOP, these homeowners must have moved into their homes before end-2011. The most recent batch of buyers who qualify probably purchased flats during the BTO offerings in 2007.

This group of buyers are incentivised to upgrade or relocate because they not only enjoyed the price appreciation of their flats from 2011 but also the implicit subsidies embedded in the prices set by HDB when they purchased their homes.

Prices of flats sold directly by HDB ranged from $60,000 to $260,000, depending on the room type, location and level (Table 1).

Table 1

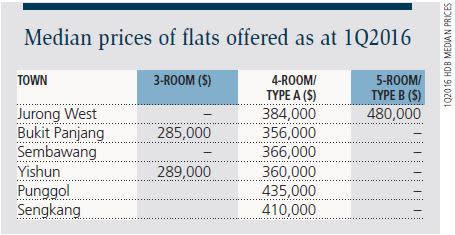

Using the median prices in the resale market in 1Q2016 as a proxy (Table 2), the average amount of cash proceeds that HDB owners might receive from selling their flats in 2016 is estimated to be $188,000. In addition, they would have built up their housing equity over time while paying their monthly instalments. This adds to their equity for home purchases.

Table 2

Armed with the cash proceeds, these homeowners can consider a number of options if they were to sell now, provided they meet the TDSR and other loan conditions. Based on our simple case study, the TDSR imposed on buyers tends to be the key factor constraining their housing affordability if they were to purchase a private home. If they were to purchase an HDB flat or EC, the amount they can afford is constrained by the 30% loan payment-to-income ratio. For instance, in our simple case study, our sample couple can afford only an HDB flat of about $750,000 if they were to apply for an HDB loan for their resale home, owing to the 30% loan payment-to-income ratio stipulated by HDB. If they purchase a private home, they can afford $1.4 million, assuming they have no other debts. The options available to the homebuyers in our case study are presented in Table 3.

Table 3

Note that we excluded housing grants in our computation. These grants are given through the Central Provident Fund accounts, and they will be refunded to CPF with interest upon sale of the property. We excluded stamp duties and legal and brokerage fees for the property purchase. A rule of thumb is 4.5% for stamp duties and legal fees, and 2% for brokerage fees for each property transacted.

Options for homeowners who bought their resale flats five years ago without subsidies Homeowners under this category have less cash proceeds than those who bought directly from HDB. Given the current low interest rate environment, most of the housing equity and HDB grants given will be refunded to their CPF savings upon sale because the CPF savings rate is much higher than the ongoing mortgage rates. In some cases, sellers do not have sufficient cash proceeds to refund their CPF savings. As a result, they might not have enough cash for renovation works. This group of homeowners would need to have substantial cash savings if they were to upgrade their homes.

Should HDB homeowners sell their flats now?

The decision to enter the market depends largely on the motivation of homebuyers — whether to purchase for owner occupation or investment. Homebuyers who purchase for owner occupation and have urgent needs tend to enter the market irrespective of the conditions. In the context of the HDB resale market, most buyers are purchasing for owner occupation, and price movements in the resale market does not move in tandem with sales. Most of the HDB home sellers have one property, and their sale and purchase decisions are usually tied together. Thus, their gains are only on paper, unless they have more than one home. If they sell during favourable market conditions, they have to buy their next home at a much higher price as well.

Nevertheless, there are anecdotes of sellers who decouple the sale and purchase of their homes. They sell their homes when the market peaks and rent a home or stay with their parents until the market bottoms out. While this option may seem viable, there are hidden costs — both monetary and non-monetary. For instance, academic literature has suggested that children living in owned homes have higher maths and reading ability, while behavioural problems are 1% to 3% lower.

The dilemma of whether to sell or buy a property under current conditions is mainly that of stakeholders who have a more flexible time schedule. On the one hand, prospective buyers prefer to wait for the market to bottom out before entering, especially when home prices are anticipated to ease further. On the other hand, the options — at least in the secondary market — in a down market will be limited, as sellers of better-quality homes tend to have strong holding power and are less likely to sell at a discount. Studies have shown that homeowners exhibit “loss aversion” and will not sell their homes at a price lower than what they purchased for. Even properties auctioned in mortgagee sales do not have the 20% to 30% discount that buyers are looking for.

These stakeholders have to weigh their investment/owner occupation motives. If they have stronger owner occupation motives, they should not wait for the market to bottom out. Rather, they should start searching for the ideal property with a long-term horizon. Investors would have to evaluate how the purchase of the investment home affects the performance of their portfolio of assets over their investment horizon. Although residential prices are expected to ease further, it may be more resilient than other assets.

How rise in number of sales launches affect resale prices

Last December, the Ministry of National Development announced that the supply of BTO flats would be raised to 18,000 units. Given that some BTO projects saw good response from second- time applicants, there were concerns that the increased supply would put more pressure on house prices.

However, if we consider the demand for homes each year, the increase is justifiable. Using the number of marriages as a proxy for HDB flat demand, there were 27,600 marriages a year in the past five years. While not all new couples will buy an HDB flat, we need to incorporate demand from singles aged above 35 who are qualified to purchase a resale flat and Singapore citizens who have met the necessary conditions. With that in mind, the increase in supply is unlikely to affect prices significantly. This is further corroborated by recent applications for BTO homes in 2015 and 2016 so far. In 2015, the number of applications for BTO flats was 42,799, according to HDB. So far this year, the two launches have already attracted 27,758 applications, versus the 18,000 units to be offered for the whole year.

While the BTO offerings divert some first-timers away from the resale market, the HDB secondary market is still supported by permanent residents, singles and families who want to stay near their parents. This is especially so after HDB introduced the Proximity Housing Grant to homebuyers.

The design and floor area of the older flats are also attractive to some households. A case in point is executive flats, which offer a floor area of about 1,500 sq ft. As at 2016, these units are priced from $650,000 to $900,000, depending on their location and furnishings. They offer good value since one has to fork out at least $1 million for a private home of the same size.

Outlook for HDB market

Sales of HDB resale flats are likely to ease because of the slower economy. There will be fewer units offered in the market as sellers are unlikely to upgrade. Accordingly, home prices are also likely to ease slightly. We anticipate the decline in demand and prices to be moderated as the bulk of the sales in the resale market are driven by the desire for homeownership.

Lee Nai Jia is director, head (Southeast Asia) research at Edmund Tie & Co (SEA) Pte Ltd. He can be reached at naijia.lee@etcsea.com.

This article appeared in the The Edge Property pullout of Issue 738 (July 25, 2016) of The Edge Singapore.

Related Articles From TheEdgeProperty.com.sg

Moderate price fall for private homes in 2Q2016

Edmund Tie & Co charts a new course

C&W sells its majority stakes in Edmund Tie & Company Holdings

JUST SOLD: Queenstown’s second most expensive HDB flat