Why Married Dual-Income Couples Should Try Living As A Single-Income Family

This article was first published on 3 October 2015 and updated with the latest information.

We love challenging societal norms. One of the main reasons for that is because we believe lives can be improved if the correct norms are being challenged.

Today, we like to challenge you (particularly, young married couples), to try spend less. In fact, if possible, we believe that the optimal aim is to try living as a single-income family, even if both of you are working.

We don’t deny that this would be an uphill task for most Singaporean couples, including ourselves. We are, on a daily basis, being bombarded with strategically crafted advertisements created for the sole purpose of enticing us to part with our hard earned money to buy whatever products or services that they are selling.

But trust us, there are many good reasons for us to challenge ourselves to live on single-incomes.

How Much Does The Average Household In Singapore Spend?

Assuming we meet a young married couple earning $3,000 per person per month, or $6,000 in total. This couple would take home a total of $4,800 per month after CPF contribution. We assume that their CPF contribution is sufficient to take care of their monthly mortgage.

The table below depicts how this income relates to actual expenditures of households in Singapore. Information is taken from SingStat.

This is a very conservative estimate (perhaps overly so), since there are many households with more than 2 working adults.

What we are going to say may not appeal to everyone. And obviously, there may be many other who will disagree with us on being able to spend so little on household expenditure in expensive Singapore.

The table above shows that an average middle-income household in Singapore spends about $4,812 per month. It also shows that the lower income households in Singapore spend about $2,570 per month. What we are suggesting here is that even though you are making middle-income type of salary, you could try to live as a lower income family.

It will be tight but as the lower income families in Singapore have shown, this is possible.

Advantages Of Spending Way Below Your Means

While spending less and drafting budgets aren’t exactly the most fun thing in the world to be doing, there are clear advantages to doing so.

You are not beholden to your jobs and at any point, one of you can leave with virtually no repercussions, assuming your spouse is still working. As a sub-point, the wife can comfortably take time off for maternity and the family can plan for what is best for their child.

With a lower month expenses, you don’t need such a sizeable emergency fund in case one or both of you lose your job(s).

Early retirement is possible through a combination of being able to save more and invest more.

Read Also: What Is Gross Monthly Household Income – And How Does It Affect You In Singapore?

Not Being Beholden To A Job

You have a job you hate and you don’t have time to find a new job because you are simply too busy at the end of each working day. You are caught in this vicious cycle. Does that sound familiar?

What if we tell you that spending less (more specifically, spending based on a single-income family) means that you could leave your current job anytime (as long as your other half remains working), and take sufficient time to find a new and better and more rewarding job without worrying about your monthly bills stacking up or going into massive debt? Would that proposition interest you?

Too often, young working adults incur too much lifestyle expenses when they first begin working and very quickly, find themselves stuck in their jobs just so they can continue sustaining their lifestyles. If you can spend less, you can retain more control of your lives. And, the best things in life are supposed to be free anyway?

Saving Less For An Emergency Fund

We always advocate that families should minimally have 6 months of expenses set aside in an emergency fund. There are two variables to this equation.

Firstly, you need to make money to be able to save. We often hear of people complaining that they are unable to save because they don’t earn enough. Fair enough, most, if not all of us, can’t control our monthly income.

However, we hardly ever come across anyone who complains that they are unable to save because they spend too much. When you think about it, it’s a little strange because expenses is the one thing that we can control after all.

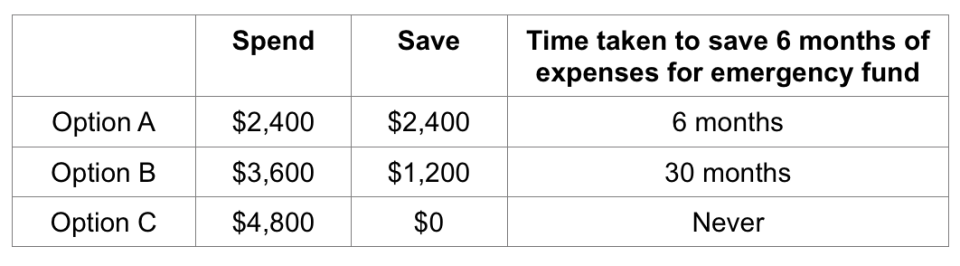

The great thing about spending just one person’s salary is that it doesn’t require you to take a long time to accumulate what you need for an emergency. Because you are spending just $2,400 each month and saving $2,400 each month, you will only need 6 months to accumulate the amount you need.

Here is a table depicting three extremely simplified spending scenarios based on a couple that takes home $4,800 in total.

By spending just $1,200 more each month, the couple would take 5 times longer to accumulate the amount they need in their emergency fund. That is because every extra dollar they spend isn’t just money being taken away from their savings, but also increases their spending and hence, requires them to have a greater amount in their emergency fund.

Read Also: Working Adults Guide To Starting An Emergency Fund – And How Much You Should Have In It

More To Invest, And You’ll Likely Be Able To Retire Earlier

The less you spend, the more you save and can afford to invest. The more you invest, the earlier you can retire.

Let’s assume that a 25-year old couple decides to invest $2,400 per month at a return of 6% per annum. Believe it or not, by the age of 50, the couple portfolio would have been worth about $1.66 million. Not too shabby for a middle-income family isn’t it?

If we assume that the couple gets a 3% dividends each year from this retirement portfolio, they would receive about $4,000 per month in passive income. That’s even more to spend in retirement than they had when they were working!

Spend Less Today, For A More Secure, Comfortable Tomorrow

Spending based on one person’s income may provide many advantages in the long run in exchange for some lifestyle adjustments today. Giving up the car, meals in restaurants and your two (or three) annual holidays may seem like big sacrifices, but this pales in comparison when you consider the extra freedom that you retain in your life by living a more frugal lifestyle.

The post Why Married Dual-Income Couples Should Try Living As A Single-Income Family appeared first on DollarsAndSense.sg.