What could a digital banking licence mean for Singtel?

What could a digital banking licence mean for Singtel?

DBS Group Research is keeping its “buy” recommendation on Singtel with a target price of $2.69, as analyst Sachin Mittal believes that the Singtel and Grab joint venture is a strong candidate for a full digital banking license.

In this JV, Singtel owns 40% of the the JVCo, while ride-hailing and payments platform Grab owns the remaining 60%. To that end, Singtel is expected to have to commit over $600 million in total to the JV in the long term.

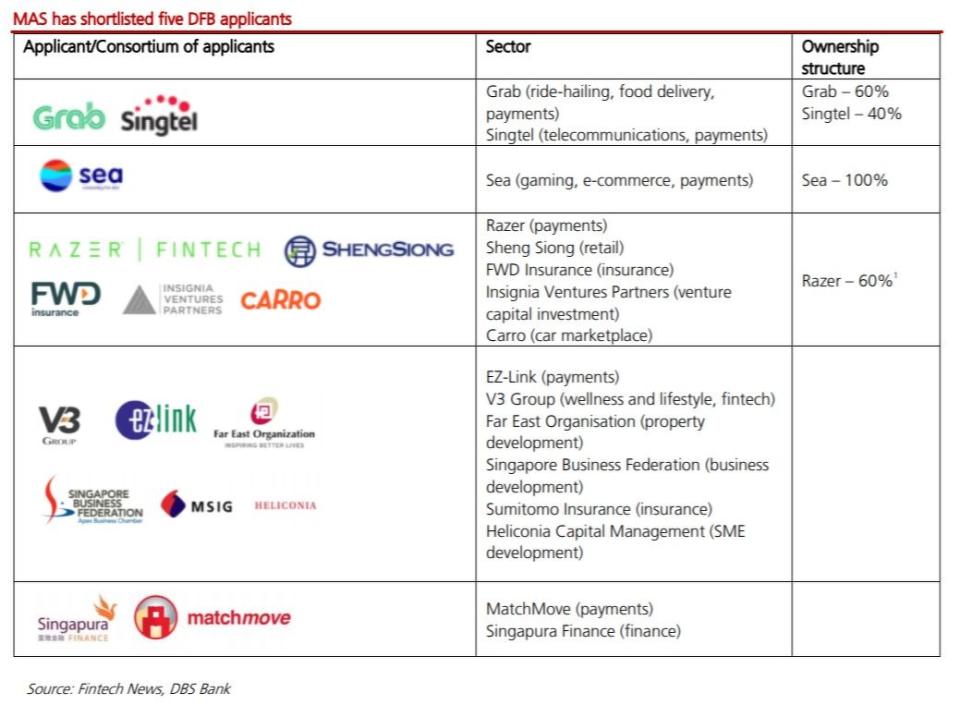

To recap, the Monetary Authority of Singapore (MAS) announced last year June that it would grant up to five digital bank (DB) licences – two digital full bank (DFB) licences to provide financial services and allow deposits to be taken from retail customers and three digital wholesale bank (DWB) licences may be issued, catering to small- and medium-sized enterprises (SMEs) and other non-retail segments in Singapore.

MAS says that the DB licences will be awarded by end-2020.

Five DFB have been shortlisted:

Of those shortlisted, Mittal is positive on the Grab-Singtel JV prospects. “Grab-Singtel JV has a potential to win 2%-4% share of the Singapore consumer market (excluding mortgages) in five-years while achieving breakeven in four to five years,” he says.

Products offered through this consortium are likely to seamlessly integrate into the daily lives of Grab’s and Singtel’s large, highly engaged customer base, according to the analyst.

Singtel has a subscriber base of 4.3 million (as of June 2020) while Grab has over 187 million users across Southeast Asia. This consortium is expected to result in several synergies, as the duo have previously been part of several digital innovations and have launched fintech products such as Dash, GrabPay and GrabInsure.

“While no details have been disclosed publicly, we think that the consortium might target Grab drivers and partner Hawker centres & food partners for unsecured loans and credit solutions given vast amount of data lying with Grab and Grab Pay,” says Mittal.

“The consortium could target to acquire 4-5% of Grab’s user base in Singapore along with 20-40% of Grab partners in three to five years, in our view. This could translate into 150,000 to 200,000 customers for the consortium. Interbank borrowings could be the main source of funding due to the lack of adequate paid capital and deposits initially,” he adds.

On the other hand, Mittal also likes Singtel as the stock is currently undervalued, especially its core business in Singapore and Australia. As also mentioned in his previous report dated Oct 19, the analyst says, “The market value of Singtel’s associates is $2.17 per share, same as Singtel’s current share price, and implies that the market is not assigning any value to its profitable core business in Singapore and Australia.”

See: Singtel's latest asset divestment to support dividends: DBS

As at Oct 27, shares in Singtel are trading at $2.10 or 25 times FY21 earnings with a dividend yield of 5.8%.

See Also:

September cheer for manufacturers but MAS warns of slow, uneven recovery

Analysts mostly positive on Mapletree Industrial Trust after 2Q results release

Singtel expected to see better associates' contribution in FY21 led by Bharti's improvement

DBS Group Research ups Singapore's FY2020 growth forecast, says recovery 'underway' but remains uneven

Rebound in Singapore's economy likely to take longer than previous recessions: MAS