Why Hong Kong pensions are so much worse than Singapore's

In its present form, Hong Kong’s pension system doesn't live up to its billing.

In May, the South China Morning Post published a letter from a reader who wrote to say that Hong Kong’s Mandatory Provident Fund should be abolished as “it has failed on multiple levels from the perspective of ordinary citizens.” Replace it with a universal basic income, he suggested.

Hong Kong was recently graded C+ in the Mercer CFA Institute Global Pension Index 2022. Being in the same category with the US, France and Spain means that MPF has “some good features, but also has major risks and/or shortcomings,” the study noted.

Still, is the MPF so bad that it should be scrapped?

I had argued in early 2019 that Hong Kong’s old-age security ought to be fortified with a state-provided pension to have any chance of a favourable comparison with Singapore’s Central Provident Fund, or CPF, which is rated B in the Mercer CFA Institute survey. (In the Asia-Pacific region, only Australia’s retirement system is graded B+. For really world-beating outcomes, one must live in Iceland.)

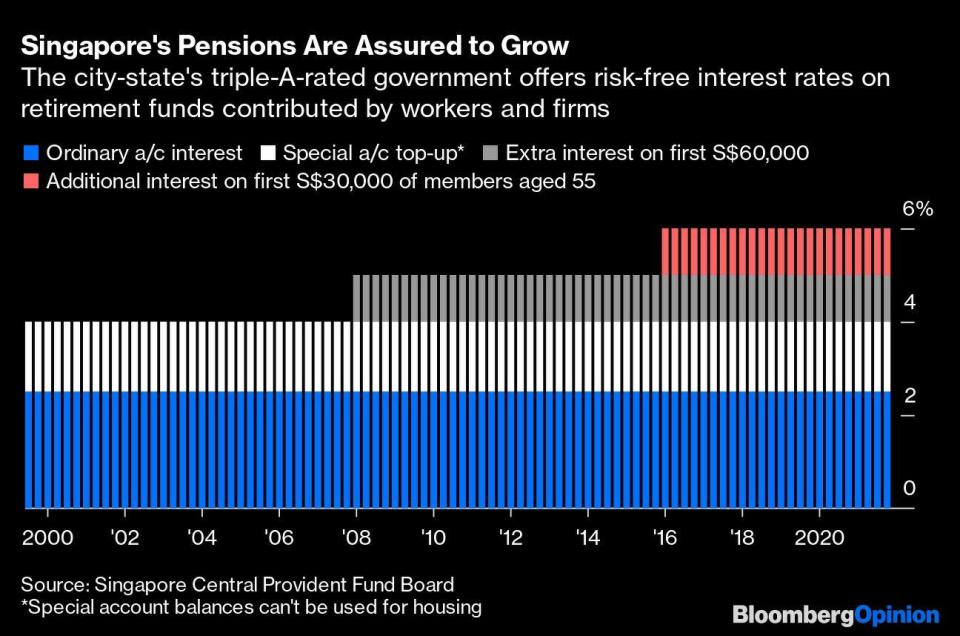

Both Hong Kong and Singapore collect defined contributions, but there the similarity between the rival financial centres ends. Singaporeans below 55 years of age mandatorily save 20% of their pay up to a salary cap; their employers funnel another 17%. That works out to about $2,200 each month. Hong Kong’s forced savings, equally shared by the worker and the firm, top out at HK$3,000 ($545.5; US$382) and comprise the bulk of MPF. Voluntary contributions, which enjoy tax breaks, accounted for less than a quarter of the money that came into the system in the June quarter.

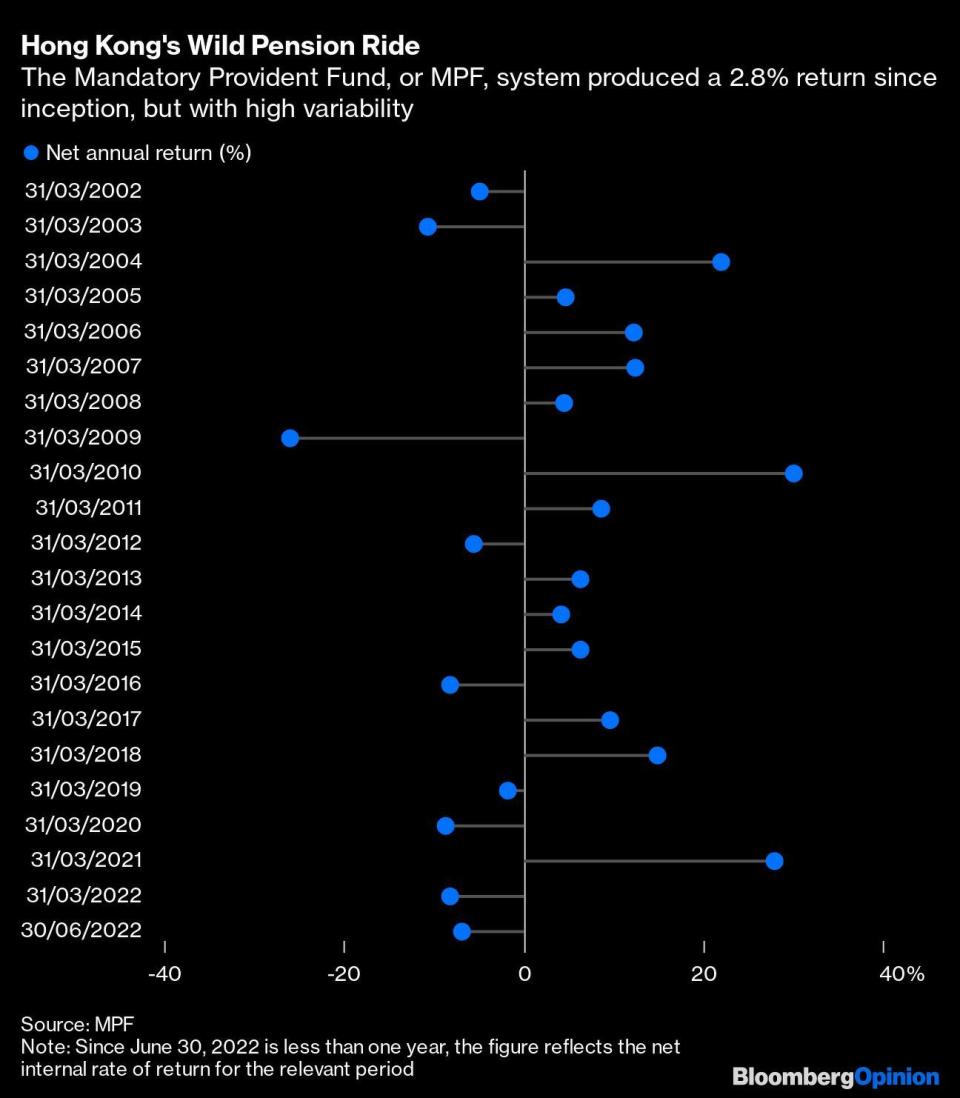

Not only do Singaporeans squirrel away four times more, their triple-A-rated government offers a guaranteed 4% return on so-called special accounts, which can’t be used for housing. (For those who want to dip into their savings for apartment purchases and mortgages, the ordinary account pays a risk-free 2.5%.) By contrast, Hong Kong’s pension outcomes are strictly a private affair: They’re determined by the performance of the funds members select from the menu offered by providers such as HSBC Holdings Plc and Manulife Financial Corp. The annualized net rate of return has been 2.8% since the inception of the MPF in 2000.

In September, total MPF assets fell below the HK$1 trillion mark for the first time since July 2020, when the pension system crossed that milestone, according to MPF Ratings. The independent researcher estimates investment losses so far this year at HK$260 billion. High inflation and rising interest rates, global recession risks, a war and energy crisis in Europe and a meltdown in China’s property industry have all added to the volatility. Plus, the average saver has a home bias. That has hurt returns this year as Hong Kong’s economy paid a price for mimicking the mainland’s aggressive stance against Covid-19 infections.

It’s unfair to judge a long-term savings vehicle by one year’s performance. However, the comparison with Singapore is too stark to ignore. The first S$60,000 accumulated in CPF accounts earns a 1% top-up interest rate. In other words, had MPF’s 4.57 million members kept their average December balance of roughly HK$255,000 in the rival city, they would have been earning 5% this year — and not losing 18%. In Hong Kong, to beat inflation, members tilt their portfolios toward equities, which exposes them to excessive risks at times like the present. Singapore, meanwhile, is helping those over 55 years of age to save and earn more so that they have a decent standard of living in their sunset years.

How does Singapore achieve high returns? The city-state borrows pension funds from the CPF Board, mixes them up with regular public debt and unencumbered assets such as money raised from selling government land. The central bank converts the whole lot into foreign currency and hands it over to GIC Pte, the sovereign wealth fund. GIC goes around the world shopping for assets — it’s hunting in Japan right now because the yen is cheap and tourism-related properties would benefit from a border reopening. Private equity has to return investors’ money after seven years. There’s no such pressure on the wealth fund. Even if GIC performs poorly in any year, the government would still pay its committed interest rate on special securities it issues to the CPF Board.

GIC came into existence in 1981 after the export-oriented economy had acquired more foreign-exchange reserves than it would need to defend its currency. Still, its first two decades were devoted largely to building organizational capacity by testing waters in liquid, public securities. Over time, GIC’s tolerance for risk grew. Hong Kong’s MPF, born three years after the city’s 1997 handover to China, has perhaps missed the chance to create a similar institutional mechanism: Almost 38% of the population is aged 55 years or older. Their best years for accumulating wealth are over. Besides, Hong Kong’s economic arrangements after 2047 will be entirely at Beijing’s discretion. So the question boils down to this: How to provide old-age security for the next 25 years?

One solution may be to make an Iceland-style, tax-funded pension the first pillar. In fact, the goods and services levy that Hong Kong has never managed to introduce could become palatable if it pays for old-age security. The provident fund stays mandatory for all employees earning more than a living wage, but the savings should be used by younger workers to offset homeownership costs, which will be a big help in a city that has some of the world’s most expensive real estate.

There’s no need to retire the MPF: It isn’t a defined benefit plan adding to systemic financial risk. But the SCMP reader is right. In its present form, Hong Kong’s pension system doesn't live up to its billing. Aping Singapore isn’t an option; Iceland looks like a more promising model.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

HK tries to reverse expat exodus with housing tax cut, new visa

Equities slow as inflation takes hold, but long-term opportunities are still available

Hong Kong to outline ambition to become top virtual asset hub

Get in-depth insights from our expert contributors, and dive into financial and economic trends