Eurozone opts to keep Greece in the family

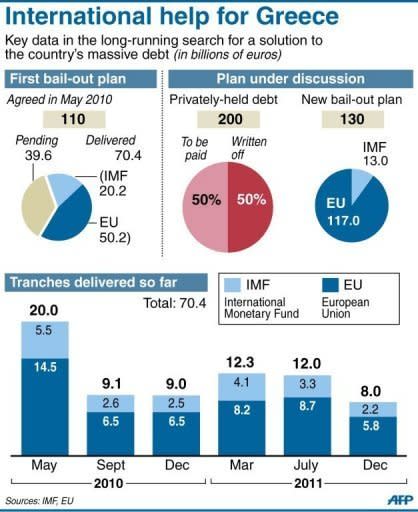

A huge eurozone rescue package agreed Tuesday saves Greece from default and keeps it in the single currency bloc under strict controls, but markets are sceptical and Greek unions are calling fresh protests. The ball is now back in Athens' court to push through legislative reforms required under the 237 billion euro deal, including an amendment of its constitution to ensure that priority is granted to debt repayments. While the euro and bond markets gave the deal a thumbs up in early trading, European stock markets fell and the single currency weakened in the afternoon as scepticism grew over Greece's ability to meet its creditors' demands. After weeks in which some in the single currency area raised the spectre of cutting Athens adrift, Italy's Prime Minister Mario Monti said the agreement represented "a good result for Greece, the markets and the eurozone." Prime Minister Lucas Papademos, who with European backing heads an emergency coalition government, pronounced himself "very happy." The chief negotiator for the private creditors now facing a 53 percent loss on their Greek holdings -- Charles Dallara of the Institute of International Finance (IIF) -- said the deal offered a sign that the troubled euro may be emerging from the danger zone. "I would not want to say that this is a definitive turning point. I do feel that it is part of a turning process," Dallara said. "You now have the seeds planted I think, firmly moving toward a restoration of confidence in the eurozone." The White House lauded the deal as important, but stressed there was more work to do. It said US President Barack Obama called German counterpart Angela Merkel to welcome "positive steps" to ease the EU's smoldering debt crisis. "The president thanked the chancellor for her leadership, and welcomed last night's agreement in Europe on a new rescue program for Greece to help reduce its debt to sustainable levels," said spokesman Jay Carney. But he added: "Additional steps should be taken," including strengthening a financial firewall that would prevent the debt crisis from spreading to larger economies such as Italy and Spain. "Progress still needs to be made," Carney said. Economists too injected a note of scepticism, focusing on the giant task ahead of Greece to get its economy growing again and also casting wary eyes on other countries that could now face pressure -- namely Portugal, Italy and even France. "Even with this agreement, most of Greece's problems lie ahead of it, not behind," said Brussels-based commentator Sony Kapoor. Luxembourg Prime Minister Jean-Claude Juncker formally announced a deal in the early hours of Tuesday, saying the "comprehensive blueprint" would "secure Greece's future in the eurozone" and safeguard eurozone financial stability. However, he spelled out a series of conditions to be met before loans of up to 130 billion euros until 2014 could be handed over. Greece has to implement certain changes by the end of February. In addition, there will be a "permanent" presence of EU and IMF officials on the ground in Athens to run the rescue programme. It is also expected to incorporate constitutional provisions for "ensuring that priority is granted to debt servicing payments." The $310 billion bailout, obtained after another 3.2 billion euros of spending cuts were rammed through the Greek parliament during violent protests, also depends on bond-holders agreeing to erase just over half the paper value of privately held Greek sovereign debt. Negotiators for the banks said this should reduce Greece's debt mountain of 350 billion euros by 107 billion euros. The eurozone will decide whether this part of the deal exchange has been successful in early March, Juncker said. The International Monetary Fund meanwhile has agreed to contribute 13 billion euros ($17.3 billion) to the bailout package, German Finance Minister Wolfgang Schaeuble said. The goal now is for Greece's public debt to fall to 120.5 percent of gross domestic product (GDP) by 2020, from the current 160 percent, taking it to what is hoped will be a more sustainable level. Athens should in the meantime be able to meet debt repayments of about 14.4 billion euros on March 20, avoiding a messy default. However, markets are concerned that the wider eurozone picture remains unclear, with analysts expecting Portugal, another fragile euro state, to need a revised bailout later this year. Berenberg bank analyst Christian Schulz raised questions about the stability of France, the European nation most heavily exposed to Greek debt. But France's European Affairs Minister Jean Leonetti told parliament that the accord would have "no repercussions on the French and for our banks," because they have "anticipated this situation" of erasing part of Greek debt.