6 Investments In Singapore That Provide Guaranteed Principal And Returns

There aren’t many investments that guarantee your principal as well as returns in Singapore. Of those that do, you need to further weed out the potential scams – i.e. investments that sound too good to be true are usually too good to be true. You can refer to the MAS Investor Alert List, providing a list of unregulated persons or companies as a first layer of check.

One other thing to understand is that when you get to enjoy such safety in your investments and visibility in your investment returns, you need to be prepared to accept a lower rate of return that is closer to the risk-free rate.

What Is Risk-Free Returns?

The risk-free return refers to a rate of return that you can expect to achieve even if you don’t take on any risk. Theoretically, there’s no such investment as there will always be some form of risk that we take on when making an investment.

Below, we look at six types of investments that you can put your money into which guarantees your principal and provides a guaranteed return on investment. This can be a good way for those who are extremely risk-averse or just unsure about investing to get started. It can also act as a springboard to start investing in riskier investments.

#1 Singapore Government Treasury Bills (T-Bill)

For us in Singapore, a good proxy for the risk-free rate can be the return that the government of Singapore, which is one of the few triple-A rated economies in the world today, pays on its 6-month or 1-year treasury bills, the shortest-term government securities available.

This is as close to the risk-free rate as you can get and the latest issuance of T-bills in September 2021 offered a median yield of 0.27% per annum, while the most recent 1-year T-bills issued in July 2021 offered a median yield of 0.28% per annum.

Treasury bills are typically useful for investors who are looking for very short-term investments of up to one year, without taking on any investment risk.

#2 Singapore Government Bonds

The Singapore government also issues longer-termed bonds, between 2 and 30 years. These bonds typically pay higher returns than the 1-year treasury bills. With all things equal, a bond with a longer maturity is typically deemed to carry more risks than the same bond with a shorter maturity period. Nevertheless, it is also regarded as close to risk-free and hence offers a rate of return that is close to the risk-free rate as well.

In September 2021 the government issued the first tranche of its SINGA bonds to finance major long-term infrastructures, such as new railway lines, coastal protection projects and other infrastructure projects that will benefit current and future generations of Singaporeans. The SINGA bonds are considered as Singapore Government Securities (SGS) bonds. The average yield of this first 30-year bond issued in September 2021 was 1.84%.

The Singapore Government Bonds offer these rates. As you can see in the chart below, the longer the bond term, the higher the yield would be as well. The 2-year government bond yield is also very similar to the 1-year treasury bill. The price discrepancy may be due to the auction date of the treasury bill.

Singapore Government Bond Term (Tenor) | Yield (p.a.) |

2 years | 0.52% (Sep Issue) |

5 years | 0.65% (Aug Issue) |

10 years | 1.55% (Jul Issue) |

15 years | 1.92% (May Issue) |

20 years | 1.77% (Aug Issue) |

30 years | 1.84% (Sep Issue) |

#3 Singapore Savings Bonds (SSB)

By now, you would have noticed a recurring theme. The investments that are most likely to guarantee your capital and your returns are fixed-income investments issued by the government.

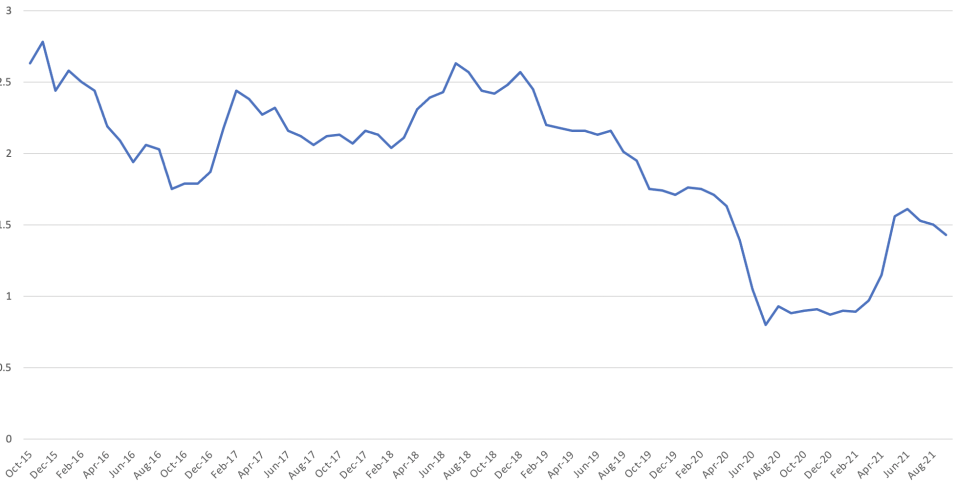

First launched in October 2015, the SSB pays a step-up interest rate each year, up to the 10th year. What this means is that the bonds pay a lower return in the beginning years, and if investors do not redeem the bond, it continues to pay a higher rate each year, until the 10th year. This is primarily to recognise the fact that investors are holding the bonds for a longer-term.

Read Also: [2021 Edition] Complete Guide To Buying Singapore Savings Bonds (SSB)

Here is the rate of each SSB issue, if you hold it for the full 10-year time frame, since its inception in October 2015.

In general, the SSB offers superior liquidity, allowing investors to redeem it at any point. This usually means that the SSB should pay out similar, but slightly lower, interest rates than other government securities that do not offer this liquidity benefit.

As depicted in the chart, the SSB interest rate yields has been on a downard trajectory since the start of 2019, but has climbed since the start of 2021.

#4 Fixed Deposits

Although not commonly referred to as an investment, fixed deposits offer you a way to earn better returns on your money rather than leaving it in a savings account or under your pillow. As a reference, the three local banks in Singapore are currently offering the following Singapore-dollar fixed deposit rates.

Bank/ Tenor | 12 months p.a. (%) | 24 months p.a. (%) | 36 months p.a. (%) |

1.15 | 0.9 | 0.85 |

0.15 | 0.2 | 0.5 |

0.1 | 0.2 | 0.5 |

Of course, there are many other banks offering their own fixed deposit schemes as well as promotional rates which can be significantly better than the board rates. Many of them, including the three above, may come with certain conditions you have to fulfil to achieve the promotional rates. While it may seem like DBS is offering the best interest rate, we also have to look at the T&Cs closely, as the 1.15% interest rate is only provided on up to $9,999. For example, those who want to keep a fixed deposit of $50,000 or more in a 12-month fixed despot, DBS’ rate is 0.05%. In contrast, UOB is paying 0.15% while OCBC is paying 0.2%

In addition, deposits with all full banks and finance companies in Singapore are covered under the Singapore Deposit Insurance Scheme, insuring up to $75,000 of your deposits in each account. All full banks and finance companies in Singapore, a total of 37 are listed on the SDIC website, are members of the Singapore Deposit Insurance Scheme.

Read Also: Beginners’ Guide To Fixed Deposits In Singapore

#5 CPF Top-Ups

To earn better interest returns, you can also consider making CPF top-ups into your Special Account (SA) via the Retirement Sum Topping-Up (RSTU) Scheme. These funds are guaranteed by the Singapore government and offer a minimum guaranteed return of 4.0% p.a. You can also make Voluntary Contributions (VC) into your Ordinary Account, Special Account and MediSave Account.

Moreover, the first $60,000 of your CPF monies, with up to $20,000 in your CPF Ordinary Account (OA), will earn an additional 1.0% p.a. in interest returns. This means your top-ups may earn up to 5.0% p.a. if you top-up your CPF SA in the early years.

You also stand to receive up to $7,000 in tax reliefs when you make RSTU top-ups into your CPF SA, as well as an additional $7,000 in tax reliefs when you make cash-ups into a loved one’s CPF SA. No tax reliefs are provided when you make Voluntary Contributions to your CPF accounts.

However, before you do this, you need to know that unlike the investments listed in this article, which can be sold or redeemed early (notwithstanding that you may lose some value when you do this), topping up your CPF SA is irreversible. You will only receive it once you hit 65 in the form of monthly CPF LIFE payouts, rather than in cash.

Read Also: Retirement Sum Topping-Up Scheme (RSTU) VS CPF Voluntary Contributions: What’s The Difference?

#6 Savings Plans

Savings plans, offered by insurance companies, especially those that are non-participating in nature, are able to guarantee your capital as well as returns. You should also note that savings plans that guarantee your capital but do not guarantee returns also exist.

When investing in a savings plan, you are typically required to lock your money over a fixed period of time or continue contributing over a fixed period of time. Not doing so may see you losing a substantial amount of the returns you expected to receive, if you are unsure about your liquidity needs for the funds you are investing.

These plans are also covered by the Singapore Deposit Insurance Scheme in Singapore and may also offer an insurance component that pays out in the event something unfortunate happens to you.

Moving On To Investments With Greater Risks

Once you’ve built a foundation or start your investing journey, you will have more knowledge and courage to make riskier investments. Riskier, but still relatively safe, investments, such as cash management accounts give you a higher return for your spare cash while still providing a high degree of liquidity.

As you progress in your investing journey and understand that taking calculated risks over the long-term can be financially lucrative, stocks, properties and other alternative investments such as cryptocurrencies or even wine may become investment options that are able to deliver significantly higher returns.

This does not mean you stop being prudent with your investments. In fact, quite the contrary, as you need to be even more prudent when you’re embarking on riskier investments. Many of these riskier investments are volatile and require you to be able to stomach, and ride out, wild price swings at times to earn good returns over the long term.

Read Also: Step-By-Step Guide to Stock Investing in Singapore

This article was first published on 16 January 2018 and updated to reflect the latest expected investment returns.

The post 6 Investments In Singapore That Provide Guaranteed Principal And Returns appeared first on DollarsAndSense.sg.