Coronavirus small businesses stimulus program off to a rocky start

On Friday, banks across the U.S. began accepting applications for low-interest and forgivable loans from small businesses under pressure due to COVID-19, though not all banks were ready or comfortable with opening their doors or their websites to take the requests.

And as of Friday morning, Bank of America (BAC) began accepting applications. The country’s largest bank, JPMorgan Chase (JPM), emailed customers on Thursday to communicate that it would not be ready by Friday to accept loan applications, though on Friday afternoon had launched a website where the application process could be started.

Treasury Secretary Steve Mnuchin tweeted Friday afternoon that more than 875 million applications had been processed under the department’s new Payroll Protection Program. Most, he said, were processed by community banks.

Elliot Richardson, President of the Small Business Advocacy CounciL, which advocates on behalf of small businesses, told Yahoo Finance that while the program’s application form is live on the Treasury Department’s website, a large percentage of lenders are not permitting prospective borrowers to submit them.

“It’s my understanding that these banks are looking for clarity,” Richardson said.

The slow rollout is causing business owners to fear that funds will run dry before they have a chance to access them.

Gary Glenn, is one of those business owners. His Glenview, Illinois S-corporation, Stitchmine Custom Embroidery, which has annual revenues around $750,000, employs four full-time workers, and is running out of free cash needed to keep his employees on his payroll. The company has taken in no new orders in two weeks and has seen several cancelled orders. In an attempt to pivot, it began making personal protective masks and T-shirts for students to memorialize graduation milestones for ceremonies that have been cancelled.

“My sole intent is not to let my employees go,” Glenn said. “They have families they have people they need to take care of. So, the idea is to have an unbroken or uninterrupted payroll, if at all possible. The challenge is that we’ve pretty much come to a standstill with orders coming in. So we really don't have any revenue coming in at this point.”

Over the phone, Glenn read an email from suburban Chicago bank, Wintrust, which Stitchmine has used for years for its commercial banking needs.

“We continue to await final guidelines from the SBA and the U.S. Treasury Department,” Wintrust’s email said. “We have learned that many of our peer institutions have decided to not begin accepting applications due to this lack of clarity... it is likely that we will follow suit with our peer institutions until we are satisfied that the guidelines that impact this process have been properly defined.”

Glenn added that he’s concerned “it's going to be so difficult or it's going to take so long to get the money that it's going to be too late.”

Who’s eligible for the loans in the first place?

Under the Coronavirus Aid, Relief and Economic Security, or CARES, Act passed on Friday, March 27, $349 billion of the law’s $2.2 trillion is being funneled into the Payroll Protection Program that will make forgivable loans available to sole proprietors, independent contractors, small business corporations, veterans organizations, nonprofits, and tribal businesses. Independent contractors and those who are self-employed may apply a week later, beginning Friday, April 10.

Deciding whether and how soon to apply are challenging questions for companies, especially given the anticipated flood of applicants that could quickly drain the pool of resources, and a race against the clock to interpret the rules, still being worked out, that will make or break whether funds may be forgiven.

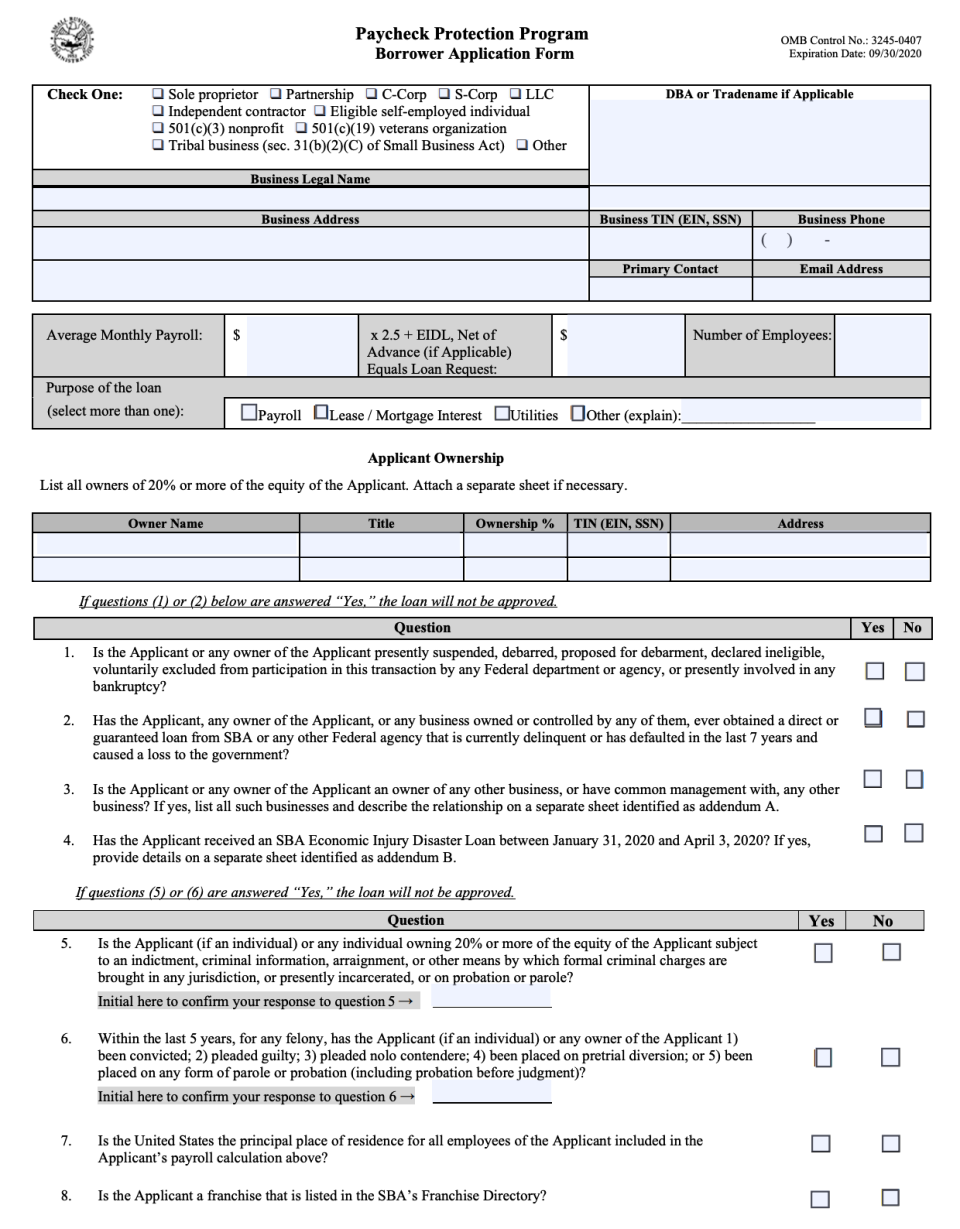

“A big question is whether or not they are eligible,” Jennifer Perkins, also a corporate partner in Kirkland & Ellis mergers and acquisitions practice, told Yahoo Finance. A copy of the loan application form can be found here.

Generally, the funds are available to organizations with fewer than 500 employees, which certify the funds are needed to support ongoing operations of the company, and will be used to retain workers and cover payroll, or to cover other specific business expenses. Certain businesses with more than 500 employees are also eligible if they are designated for an exception under the North American Industry Classification System (NAICS). In addition, some entities that share common ownership may be excluded from forgiveness eligibility.

“One of the issues is there’s an affiliation test. If you pick up affiliates, you may not qualify for the requisite size test. It’s one of the big questions we’ve been facing,” Perkins said.

Those businesses that are eligible can tap up to a maximum amount of 250% of their trailing 12-month average for monthly payroll expenses, capped at $10 million. Generally, interest rates for the loans are set at 1%, though flexibility in the legislation permits lenders to assess as much as 4%, and prescribe their own underwriting standards. Payments are deferred for six months from the date the loans are disbursed. Murray said more clarity on rate setting standards is expected to come within the next few weeks.

Treasury Secretary Steve Mnuchin announced Thursday evening that the interest rate had been raised from 0.5% to 1% after small banks said the lower rate was too low. In addition, banks requested that their due diligence requirements for anti-money laundering be relaxed and that provisions be added to relieve banks from liability for borrowers who submit fraudulent information in applying for the loans.

Loan proceeds, regardless of whether a business owner is seeking for loan forgiveness, can be used to fund payroll costs, costs related to continuation of group health care benefits during periods of paid sick, medical or family leave, as well as employee salaries, commissions, or similar compensation, Murray said. Proceeds may also be used to pay interest on mortgage obligations (and not principal payments), rent (including rent under lease obligations), utilities, and interest on debt incurred on or before Feb. 15, 2020.

Another portion of the legislation that remains unclear is whether health care benefit expenses, aside from those paid to cover periods of coronavirus-related paid sick, medical or family leave, will be forgiven.

‘They really just want to work with existing clients’

Under the CARES statute, rather than applying for loans through the Small Business Administration, applications must be filed through a participating bank.

“Small employers are going to be able to apply through their commercial banks, so their regular old bank,” Berman said.

That could create a challenge for companies that lack existing business accounts.

“One thing we are finding is that banks are willing to lend only to clients with existing relationships,” Murray said. “And the reason why is that they have to run client checks on all of their new clients. So, because client checks take a long time, in order to circumvent a lot of the paper processing and time, it is more efficient to work with existing clients.”

A starting point for business owners without bank relationships, Murray said, is a resource on the SBA’s website that lists the top 10 most active small business lenders for local regions across the country. The Treasury Department has also published a resource page for borrowers.

Asked whether she expects there to be enough money in the fund to support applicants’ requests, Berman said, “I think the program's going to run out of money very, very quickly.”

How Payroll Protection Program loan funds can be forgiven

While small businesses can use loans for a number of purposes under the new coronavirus stimulus law, the money will be forgiven only if these businesses use it for specific purposes.

To calculate the amount of forgiveness, business owners can look to current guidance that states forgivable portions will include qualifying payroll costs, payments of interest on any covered mortgage obligation, payments of rent, and payments on utilities, Jessica Murray, a corporate partner within Kirkland & Ellis’ M&A practice, told Yahoo Finance.

“If they spend it on other things, it's not going to be forgiven,” Jen Berman, CEO of MZQ Consulting, LLC and employee benefits attorney with Holder Law Group, told Yahoo Finance.

Berman also said that forgiveness provisions apply only to money spent during the first eight weeks of the loan. “Employers’ loans are not going to be forgiven if they hold onto the money,” she said. Unforgiven portions of eligible loans must be repaid under the terms of the original loan.

Loan forgiveness is also dependent on maintaining prior staffing and compensation levels, Berman said. If employers decrease their staff count below Feb. 15 levels, the forgivable amount decreases proportionally based on how many workers were terminated.

In addition, forgivable amounts decrease dollar for dollar for compensation reductions that exceed 25%. However, employers have an opportunity to regain forgiveness eligibility by hiring staff. Loan funds used to pay employees whose positions are reinstated by June 30, 2020 will again become eligible.

Alexis Keenan is a reporter for Yahoo Finance and former litigation attorney.

Follow Alexis Keenan on Twitter @alexiskweed.

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn,YouTube, and reddit.