Rising Oil Short; Specs Left Blindsided in Natural Gas and Coffee

Saxo Bank publishes two weekly Commitment of Traders reports (COT) covering leveraged fund positions in commodities, bonds and stock index futures. For IMM currency futures and the VIX, we use the broader measure called non-commercial.

This summary highlights futures positions and changes made by speculators such as hedge funds and CTA’s across 24 major commodity futures up until last Tuesday, September 15.

The Bloomberg Commodity Index rose by 0.6% with price gains seen in all but four of the 24 major futures market tracked in this report. The change was in response to a weaker dollar, improved risk sentiment as U.S. mega cap stocks bounced and not least continued strong demand from China where some key economic data surprised to the upside.

Rising prices saw hedge fund demand for commodities resume with all sectors apart from energy and softs seeing net buying with the total net-long rising by 4% to 1.84 million lots. The grain sector led from the front with corn and the soybean complex continuing to see strong buying interest while all metals led by copper and gold were bought.

Energy

Position changes across the energy sector were particularly interesting, not least considering some of the market developments that unfolded following last Tuesday. Crude oil was mixed with a 25.9k lots increase in WTI and a 39.9k reduction in Brent reducing the combined long by 3.5% to 376.7k lots, a five-months low. This before Saudi Arabia’s warning to OPEC+ cheaters and short-sellers helped oil to its best week since June. Since July when fundamentals, but not the oil price, started to weaken, the gross short held by funds in WTI and Brent crude has more than doubled to reach 248k lots.

It was this development that the Saudi oil minister saw as a worry but also an opportunity to force the price higher through short-covering. While short sellers may move the market for a short period of time, fundamentals will always be the main driver. And while the recent 15% correction in Brent crude oil helped to bring the price more in line with current fundamentals, a recovery from here needs more than verbal intervention, despite it coming from the world’s biggest producer.

Natural gas bulls found themselves caught on the wrong side of the market after increasing their net-long in four Henry Hub deliverable futures and swap contracts to the 325k lots, the highest since May 2017. Lower demand triggered by lockdowns and Hurricane Sally disruptions impacting both demand and exports helped drive a bigger-than-expected weekly inventory build, As a result the price cratered before finding support at a key technical level below $2/MMBtu.

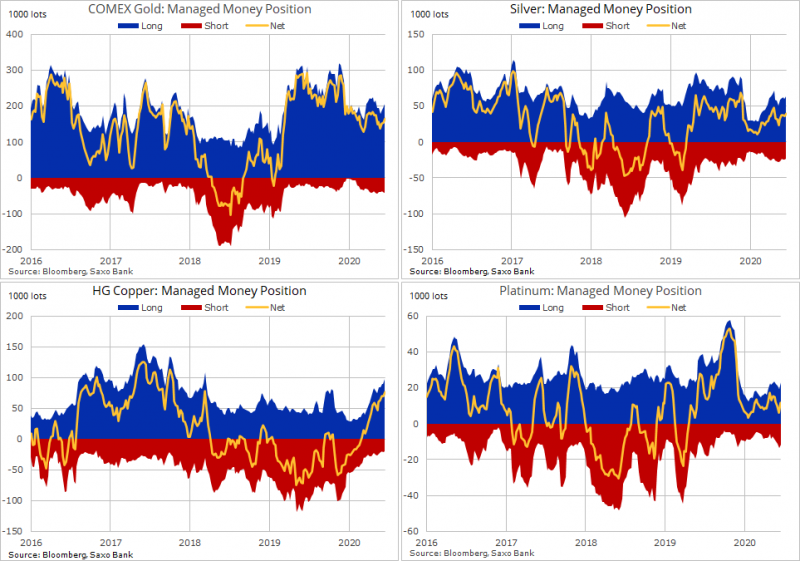

Metals

Despite being stuck in neutral, gold and silver bulls added length to both contracts. Signs of an improved outlook for platinum helped drive a near doubling of the net-long to 11.5k lots. Copper buying continued with the price being supported by strong Chinese demand and falling global inventories. The net long reached 76.7k lots, the highest since June 2018.

In our latest Commodity Weekly, we described gold as being passive given that most of the recent price impact has come from its current and unusual positive correlation to the risk appetite being dictated by U.S. mega-cap stocks. Correlations, often picked up and strengthened by algorithmic trading systems, work until they don’t. With this mind an interesting week awaits given the risk of a deeper stock market correction following Friday’s week close on Wall Street.

Agriculture

The grain sector led by corn and the soybean complex continues to be bought, thereby defying the seasonal trend which tends to see crops being sold ahead of U.S. harvest. The top global buyer China continue its record pace of soybeans buying as it seeks supplies to feed a post African swine fever rebuild of its massive hog herd.

Soft commodities were mixed with the sugar long being reduced for a second week while the Arabica coffee net-long reached the highest since November 2016. This before suffering its worst week in 22 years on reports that warehouses in Brazil, the world’s biggest grower and exporter, have never been this full. Lockdowns and the work-from-home phenomenon keeping consumers away from cafes and restaurants.

For a look at all of today’s economic events, check out our economic calendar.

Ole Hansen, Head of Commodity Strategy at Saxo Bank.

This article is provided by Saxo Capital Markets (Australia) Pty. Ltd, part of Saxo Bank Group through RSS feeds on FX Empire

This article was originally posted on FX Empire